|

The time to rethink three widely believed, but outdated management ideas is long overdue.

1. There are “good” and “bad” industries In the late 1970s, Michael Porter’s seminal article on business strategy -- How Competitive Forces Shape Strategy -- established five industry characteristics to explain why some companies are inherently more profitable than others. Porter advised managers to seek out businesses with strong bargaining power over buyers and suppliers, low threats of entry from similar or substitute products, and minimal competition, giving rise to the notion that there are “good” and “bad” industries, more or less conducive to attractive financial results. Take airlines for example, plagued by intense price competition, high structural costs and fickle customers. Most airlines historically failed to earn their cost of capital, and every major legacy carrier has gone bankrupt -- at least once. Who would want to enter such a fraught industry? But if structurally challenged industries are destined to suffer, how can one explain that Southwest Airlines’ market cap since 1980 has grown more than four times faster than the S&P 500 and more than 90 times faster than the airline sector as a whole? If a company’s choice is either to enter a poorly performing industry, playing by the same rules as incumbent market leaders, or to stay out of the business entirely, Porter's advice is well taken. But there’s a third choice: recognizing opportunities to address poorly served customers by playing by a different set of rules. Southwest Airlines initially focused on passengers who neither valued, nor were willing to pay for a broad range of amenities offered by legacy airlines, instead delivering no-frills, efficient and friendly one-class service. Similarly, companies like Casper, Costco, Netflix and Warby-Parker have attacked sources of customer dissatisfaction and/or high costs to prove that there’s no such thing as a bad industry, except if you’re an incumbent mired in an outdated business model. 2. The objective of management is to maximize shareholder value. Perhaps no management principle is preached more dogmatically than that management’s objective should be to maximize shareholder value. But this belief has led too many executives to focus on boosting quarterly earnings and stock prices with actions that compromise long-term growth -- a serious problem that’s been getting worse. For example, 80 percent of CFO’s recently reported that they would cut R&D spending if their company risked missing a quarterly earnings forecast. Moreover, S&P 500 companies have spent an unprecedented $3 trillion on stock buybacks over the past five years, partly at the expense of R&D, capital expenditures for expansion, workforce training and other value-creating activities. Share buybacks increase a company’s short-term EPS – that’s just math -- but there is growing evidence to suggest that excessive stock buybacks can undermine long-term value creation. The real issue here is that maximizing shareholder value should be the outcome, not the driver of management priorities. Corporate strategy should be guided by a customer-centric corporate purpose, a clear articulation of the time horizon for planning, decision-making and capital allocation, and how tradeoffs between stakeholder interests should be resolved. As an example, Jeff Bezos’ first letter to shareholders clearly articulated that Amazon would prioritize long-term market leadership over short-term profitability, and that the company would relentlessly focus on customers. By consistently putting customers at the center of Amazon’s strategy and new business development, the company’s market cap has increased almost 1,000X since its IPO. Customers and shareholders have been exceptionally well served by CEO Bezos’ overarching commitment to a long-term customer-centric corporate purpose. 3. Mature businesses inevitably decline Recent research has found that less than 15 percent of Fortune global 100 companies have sustained above-market growth over multiple decades. Does this suggest a Darwinian form of corporate evolution where large corporations are destined to decline? Those who question the feasibility of long-term growth point to three seemingly immutable marketplace constraints:

These “laws” are not only flawed, but they could become a self-fulfilling prophecy of corporate failure. After all, if managers truly believe that long-term growth is impossible, they will seek to protect and harvest current assets and customers for as long as possible. But such an approach—playing not to lose, rather than playing to win—only serves to hasten the decline of incumbent market leaders, as Kodak, Blockbuster, Sears and others have painfully discovered. But there are counter-examples, where businesses have continued to prosper by maintaining the same core values, entrepreneurial spirit and adaptability that led to their success in the first place:

Amazon became the fastest company to exceed $100 billion in sales last year following this approach. Over an even longer term, Johnson & Johnson and 3M are still outpacing overall GDP growth more than a century after their founding. Long-term profitable growth and shareholder value creation is possible in all industries – good or bad.

0 Comments

Being the CEO of a publicly traded enterprise requires a delicate balancing act to keep multiple stakeholders happy, namely shareholders, customers and employees. Dave Barger has been walking this tightrope for seven years as CEO of jetBlue, doing an admirable job building a profitable, growing airline that customers love to fly. This year, jetBlue earned the J.D. Power award for highest customer satisfaction among Low Cost Carriers in North America for the 10th straight year, reflecting the airline’s numerous customer-friendly perks:

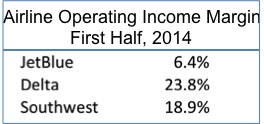

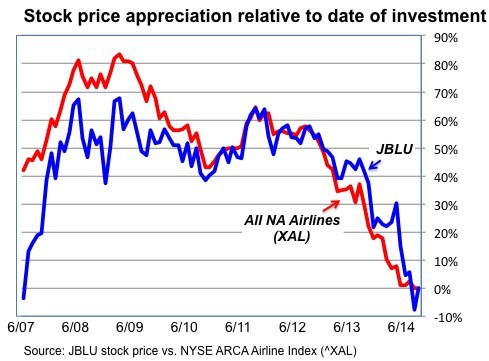

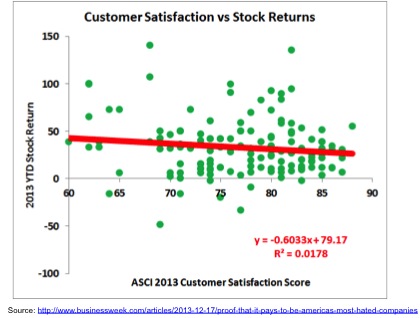

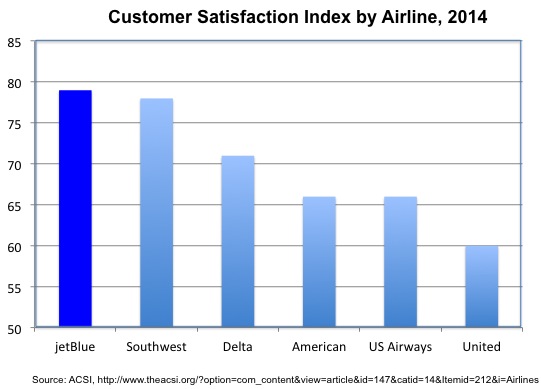

According to Bloomberg BusinessWeek, “several analysts have consistently suggested the shares are depressed because of Barger’s focus on passenger-friendly initiatives that leave shareholders at a disadvantage.” Fortune Magazine echoed these sentiments, reporting “above all, {analysts} hate that JetBlue provides the most leg room of any domestic U.S. carrier in coach, with a seat pitch of 33 inches standard. By comparison, the legacy carriers have cut their seat pitch in coach down to 30 inches, which has allowed them to stuff more seats on their planes… {Analysts} view Dave Barger, JetBlue’s chief executive, as being “overly concerned” with passengers and their comfort, which they feel, has come at the expense of shareholders.” Wolfe Research chimed in with additional advice to management: “JetBlue has ample opportunities to unlock value including a first checked bag fee, increasing seat density, cutting capex, dropping hedging, simplifying the fleet, and overbooking… to name a few.” Some analysts such as Helane Becker of the Cowan Group have gone even farther, openly calling for Barger’s head: “We believe a management change would lead to a change in philosophy and likely morph the model similar to one of Spirit Airlines although not as extreme.” This week, Wall Street naysayers got their wish, as jetBlue announced that Barger’s contract would not be renewed. In February, Robin Hayes, jetBlue’s COO will succeed Barger as CEO, perhaps presaging a concerted pruning of jetBlue’s signature passenger-friendly perks. This melodrama is reminiscent of Wall Street angst towards Amazon, where many analysts also feel that CEO Jeff Bezos has also been putting the welfare of customers ahead of shareholders. For example, Slate columnist Matthew Yglesias has called Amazon ”a charitable organization being run by elements of the investment community for the benefit of consumers.” Since when has superior customer service become viewed as a management liability? CEO’s like Dave Barger and Jeff Bezos have managed their companies with a decided bias towards long-term value creation, brand distinctiveness and customer loyalty, rather than short-term profit maximization. In this regard, Barger’s track record is actually considerably better than assessed by jetBlue’s critics. In May, 2007, Barger inherited a seriously over-extended airline that was reeling from an existential crisis of mortifying customer service meltdowns. Barger had to engineer a turnaround during a severe depression that wreaked havoc on airline balance sheets and income statements for at least three years, ultimately driving American, Frontier, Aloha and others into bankruptcy. But by 2011, the results of Barger’s transformation of jetBlue were clearly evident. The figure below compares jetBlue’s stock price appreciation vs. the North American airline industry as a whole during Barger’s tenure. As shown, stockholders who invested in JBLU on or after January 3, 2011 have enjoyed returns at or mostly above the industry as a whole through September, 2014.  Nonetheless, many on Wall Street have appeared to lose patience with Barger’s inability to convert industry leading levels of customer satisfaction into even higher growth in revenue and profits. Dave Barger is not alone in struggling with this challenge. One would like to believe that superior customer satisfaction is a competitive advantage that can help drive higher customer loyalty, word-of-mouth referrals, increased new customer acquisition, all at higher prices and profit margins. In reality though, demonstrating this linkage has proven difficult for many companies, and at best requires a long timeframe to make the case. Moreover, contrary examples abound. For example, companies with strong monopoly/oligopoly positions often exploit their market power to achieve high margins, despite horrific customer service. Take Time Warner Cable (TWC) for example, a perennial rock-bottom loser in customer satisfaction studies. Despite widespread customer abuse, TWC’s share price has grown >250% over the past five years. More broadly, the American Customer Satisfaction Institute conducts annual surveys of customer satisfaction across multiple industries using a common battery of metrics. Comparing company-specific customer satisfaction measures for 146 companies in 2013 with their stock price appreciation during the year yields the following discouraging results.  There is virtually no relation between a company’s measured ability to satisfy customers and its stock price appreciation. In fact, a regression between these two variables yields a slightly negative relationship. As noted at the outset, managing a complex enterprise requires a delicate balancing act to serve the often-competing interests of customers, shareholders and employees.[1] jetBlue undoubtedly can and will find additional mechanisms to raise revenues in the months ahead, but hopefully will do so in a manner consistent with its customer-friendly brand persona that has distinguished the airline since its founding. Calls for jetBlue to jam more seats into their aircraft and to mimic standard industry practice of charging fees for every conceivable service would render jetBlue no different from its peers, whose track record in delivering satisfactory customer service is quite poor. As shown below, jetBlue is currently a US industry leader in airline customer satisfaction.  jetBlue has invested heavily in creating an exceptionally strong customer franchise, built on a solid foundation of valued service. The challenge now is to determine how to extract more value from this strong position, without losing jetBlue’s brand essence or corporate soul. Some sage advice from Michael O’Leary, CEO of low cost airline Ryanair is apropos here: “If you don’t approach air travel with a radical point of view, then you get in the same bloody mindset as all the other morons in this industry. This is the way it has always been and this is the way it has to be.” Maintaining meaningful differentiation is essential for jetBlue to build on its distinctive brand character. Finding the right tradeoffs between increased revenue realization and valued customer service offerings will continue to be a delicate balancing act for jetBlue’s new CEO. _____________________________________________________ [1] In April, jetBlue’s pilots voted to join the ALPA union, highlighting another conflict in balancing the objectives of management and the company’s stakeholders. Imagine you’re a brand manager for a consumer packaged goods product, clawing for tenths of a percent of market share against aggressive national and store-brand competitors. The pressure to add product line extensions are constant and seemingly compelling:

Examples of product line proliferation abound:

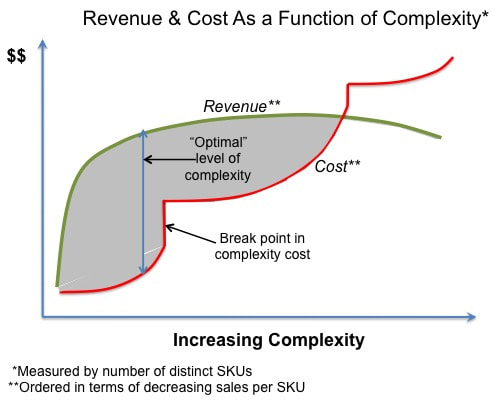

The tech sector also often falls prey to allowing excessive product-line complexity to weaken brand images and value propositions, as exemplified by Evernote. Founded in 2008, Evernote is a cross-platform, “freemium” app designed for note taking and organizing and archiving personal information. In other words, Evernote is designed to help individuals and work teams store and retrieve any information in any format on whatever devices they happen to be working on. By 2013, the company seemed to be on a roll; it had registered eighty million users and attracted over $300 million in investment from venture capitalists who valued the company at one billion dollars. But over the next two years, the company ran into trouble. In 2015, Evernote laid off nearly 20 percent of its workforce, shut down three of its ten global offices and replaced its CEO. It turns out that the vast majority of Evernote’s users only signed up for the free app and didn’t see enough value to upgrade to a paid subscription. Struggling to generate revenue, Evernote lost its focus and continuously released new products that added complexity, and often performed poorly. The company developed so many features and functions that it became increasingly difficult to explain to newcomers or even veteran users exactly what the product was. As Evernote’s former CEO Phil Libin explained, “people go and they say, ‘Oh, I love Evernote. I’ve been using it for years and now I realize I’ve only been using it for 5 percent of what it can do.’ And the problem is that it’s a different 5 percent for everyone. If everyone just found the same 5 percent, then we’d just cut the other 95 percent and save ourselves a lot of money. It’s a very broad usage base. And we need to be a lot better about tying it together.” Evernote wound up spreading itself too thin and lost sight of its core identity and primary consumer value proposition. To avoid this common management trap, let’s pause for a reality check on the true impacts of product complexity. The harsh reality is, the vast majority of product line extensions do not make financial sense. Virtually every management consulting company has an online white paper outlining their approach to dealing with the problem of excessive product line complexity. Try Googling “Product Complexity + _______” and you’ll see what I mean from McKinsey, BCG, Bain, Booz, Accenture, AT Kearney , Roland Berger et al. Academics have also weighed in with innumerable scholarly studies on the same issue. If you’re not familiar with the literature, I’ll spare you the effort by recounting four main takeaways:

These solutions are analytically elegant, mathematically precise and rigorously prescriptive. Have the quants really provided an viable approach to avoid the pervasive challenge of excess product line complexity? Actually, no. The problem is that these efforts typically treat the symptoms but not the root cause of excessive product line complexity. Unless companies address the underlying drivers of bloated product lines, they are likely to slip back into bad habits after a crash complexity reduction initiative. Not unlike yo-yo diets, when it comes to excessive product line complexity, recidivism rates are quite high. Moreover, technocratic solutions to optimize SKU counts overlook the profoundly more important link between product line complexity and overall business strategy. Both these points warrant explanation. Why do companies tend to add too much product line complexity? Marketing professionals pride themselves on their creativity and responsiveness to evolving customer needs. The urge to pursue new market opportunities and/or to respond to competitive threats are considered hallmarks of strong management. Consider for example the following rationales a brand manager might use to justify product line extensions:

Fundamental strategic choice: broad market coverage vs. targeted distinctiveness By this rationale, Apple should have responded to Samsung’s introduction of a large screen smartphone a long time ago. And Chipotle should have added a breakfast burrito. And In-N-Out Burger should have tried to appeal to new customers with a variety chicken, fish, egg and sausage menu items. What’s wrong with these companies?! Each of these companies has made a concerted choice to limit the range of merchandise they bring to market, focusing instead on delivering dominantly superior products in selected categories. Limiting product complexity thus lies at the very core of these companies’ business strategy. Their success — each has significantly outperformed sector competition — is driven as much by what they are NOT willing to do as by what they are willing to pursue. Take In-N-Out Burger for example. When is the last time you heard anyone rave about the taste of McDonald’s cheeseburgers in the same reverential terms as In-N-Out’s customer evangelists? Why is that? On the surface, both fast food chains are selling similar products at similar price points. But In-N-Out burgers taste better because:

Unlike In-N-Out, whose only entrée is hamburgers, and who restricts store hours to reflect minimal menu offerings and who limits geographic coverage to territories where the quality of locally sourced food items can be strictly controlled , McDonalds has chosen to compete on the basis a broad menu choice, global store ubiquity and extended service hours (often 24X7). But carrying such a wide array of food products around the globe complicates McDonalds’ logistics and service operations, requiring bulk shipments of frozen food products, in-store freezers, and pre-cooked orders kept warm by heat lamps in each establishment. The resulting quality differences are very real, dictated by structural differences in the underlying product line strategies.  This isn’t a case of a right vs. wrong strategy (both have been successful), but simply a reflection of two companies that have chosen to compete on very different terms. The fact remains, product complexity DOES affect quality, and the choice of ever-expanding line extensions is never without adverse consequences. Chipotle provides another example of competing on the basis of limited product complexity. In a recent article, Fortune Magazine noted that: “the Chipotle menu is limited to four core basics, but it offers a range of garnishes like salsa and cheese and guacamole that can produce scores of combinations. Chipotle serves neither dessert nor coffee (too complicated). There’s no ‘dollar menu’ or ‘limited time offers’ (too gimmicky). And While the Dulles Airport restaurant serves scrambled eggs for breakfast, Chipotle has declined to begin breakfast operations in any of its other 1,150 restaurants.” Chipotle’s approach also demonstrates the power of “versioning”, wherein a company sharply limits its core product line offering (to control costs and enhance quality), but still caters to varying consumer tastes with low cost add-ons and accessories which are simple to provide. Chipotle’s product line strategy was highly successful in the fast casual restaurant category, propelling the company's stock to grow nearly 40 percent per year during the first five years of this decade. But a series of food poisoning outbreaks in 2015 shook customer and shareholder confidence in the company's quality control processes, from which Chipotle has yet to fully recover. Less Can Be More Determining optimal product line strategy is not strictly an analytical exercise to be turned over to technocrats armed with elegant analytical models. While companies should certainly seek to selectively thin out non-performing product lines over time, a far more important strategic imperative is choosing the basis upon which your company wishes to compete: broad market coverage vs. targeted product superiority. For companies like In-N-Out Burger, Chipotle’s, Apple and many others, there is no such thing as a free lunch. These companies could not have consistently achieved product superiority without explicitly choosing to limit the range of their product offerings. When it comes to product line complexity, less can be more.  Let’s be clear; the world does not need another article pounding Ron Johnson for his ignominious fall from grace. And so I won’t. Except to use this painful episode as a “teachable moment,” rather than just gratuitous schadenfreude. So what have we learned from JCP’s failed strategy? In broadest strokes, it’s that a strategy flawed in both concept and execution has little chance to succeed. Let’s start with a reminder that JCP had to do something to change its game, which is why the Board reached out to a proven executive who had helped transform retailing at Target and Apple. Prior to Johnson’s arrival, JCP had become the somewhat dreary champion of promotion-driven selling, with predictably damaging impacts on the company’s financial performance and image .

By all accounts, Johnson is smart, hard working and decisive and it didn’t take long for the new CEO to stake out a bold and transformative strategy, defined by three major initiatives:

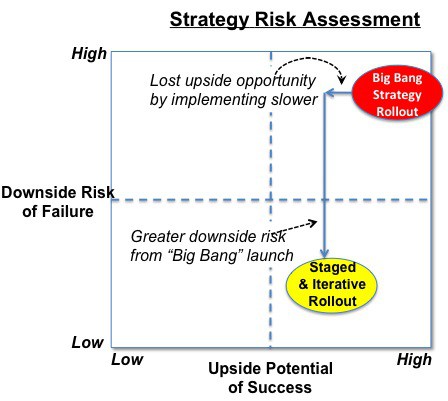

So let’s try throwing Johnson another lifeline. We’ve already noted that Johnson had to take bold, imaginative action. And he’s certainly not alone in radically transforming a sick company by aggressively rolling out an ambitious but largely untested strategy. For example, nearly thirty years ago, Nicolas Hayek raced to implement a national rollout of Swatch in the US, ignoring pilot tests indicating little consumer interest in his boldly fashioned creations from Switzerland. And of course Steve Jobs was famously dismissive about the need for market research or pilot tests before launching massive rollouts of the iPod/iPhone/Tablet. Needless to say, Swatch’s and Apple’s product launches achieved runaway and enduring success. And Ron Johnson was there, at Apple, close to the throne of the master! So little wonder that Johnson would take a page out of Steve Jobs’ (and Hayek’s) playbook to transform JCP by going bold, going big and going fast!! So why are Jobs and Hayek regarded as geniuses and Johnson a goat? Was Johnson just unlucky? On the other hand, maybe Jobs and Hayek were just lucky, and not deserving of their reverential acclaim. Bad luck or bad strategy; which is it? I’ve run out of lifelines and can no longer cut Johnson any more slack. The reality is strategy iscontextual. The fact that a particular strategy worked well in one context most assuredly does not mean that it will thrive in another. There are profound differences between the circumstances surrounding the launches of Swatch and Apple’s innovative consumer entries that simply don’t carry over to JCP’s situation. An understanding of these differences — had JCP taken the time to think it through — would have indicated ex ante that JCP’s commitment to a rapid national rollout of an untested strategy was unwise, unnecessary and breathtakingly risky. Let’s take the flaws in Johnson’s strategy one at a time. 1. The company never demonstrated compelling evidence that JCP’s customers were clamoring for its new strategy; and relatedly, JCP did not or could not articulate the benefits of its strategy in terms that were easily understood by its customers What made JCP think that its consumers hated sales promotions? After all JCP had trained their consumers for over 100 years to expect items on sale. One could surmise that JCP catered predominantly to “bargain hunters” for whom finding an unexpected bargain was part of a game that its customers felt they could always win at JCP. Ron Johnson changed the rules of a game that too many of his customer were enjoying and winning. As same store sales stats soon confirmed, customers either didn’t understand or didn’t like “fair and square pricing”. Either way, they voted with their feet and not their pocketbooks to shop elsewhere. So what is “fair and square pricing?” I put this question to my MBA class this week, and as expected found that JCP had done a poor job clearly communicating its structure and intent. One student correctly suggested that “it had something to do with less reliance on sales promotions.” Fair enough, but to be effective, JCP had to not only say what they were not going to do, but also to clearly explain what made “fair and square” better than what consumers had become accustomed or at least inured to for decades. And on that score “fair and square” pricing turns out to be pretty complicated and confusing. Here’s a primer:

In contrast, consider Swatch’s launch strategy which also was seeking to create a brand centered around value and style. With the acknowledgement that transparent pricing is easier to implement in a company with a few dozen rather than a few thousand SKU’s, here’s Swatch’s pricing approach: All watches — no matter how popular, no matter how new to market, and no matter what rock star designer inspired the creation — will be priced at $40. And that same $40 price tag will stay in force not for one month, or for one year, but for a decade. The same simple price strategy extended around the world, with prices set at 60 DM in Germany and 7,000 Yen in Japan. That’s how you create a brand that meaningfully conveys style and value! One could also argue that by moving its merchandise focus upscale, further away from Sears and WalMart, JCP was distancing themselves from their core customer base in search of new clientele already well served by brands well known for higher quality merchandise — e.g. Macy’s, Bloomingdales and Target. Along with the new pricing scheme, did the JCP really think it its new merchandising strategy would gain more new customers than it risked losing during their strategic transition? Apparently so. 2. JCP raced to implement its strategy on a national scale with no regional pilots to iteratively test and refine new concepts As already noted, there are some inspirational examples of companies that also made big bets on untested big bang launches that paid off. So why pick on JCP on this score? The companies cited earlier operated under three profoundly different circumstances that do not apply to JCP.

JCP was fighting for current market share within a well defined industry structure, not creating new markets. It’s strategic direction clearly risked alienating its current core customers, and there was no particular reason that the strategy would have been seriously compromised by a more deliberate and staged implementation incorporating testing and iterative refinement. After all, one could argue that Macy’s, Bloomingdales and Target were already occupying the very same space JCP was trying to break into, so there was nothing particularly shocking or new about their brand aspiration. Given JCP’s strategic context, Ron Johnson’s strategy reflected exceptionally poor risk management. Ask yourself this: did the upside potential of a big bang success more than offset the downside risk of failure? As viewed in this risk/reward assessment grid, the answer is decidedly not!  Lessons Learned As a parting shot, two salient lessons learned emerge from the JCP story.

We’ll never know whether Ron Johnson’s strategy would have eventually proved itself in the marketplace, but we do that he ended his career with a bang and unnecessarily put his company in grave peril. Imagine this scenario. Your 103 pound slobbering Labrador Retriever Goofy (name changed to protect the guilty) is sitting around the house one day bored and hungry — a perpetual state of being. For no particular reason (is there ever?), he jumps on the couch and stares at you with a self-satisfied grin. “No! Off!”, you urge, but Goofy stands pat with a defiant tongue dangling well below his jowls. Thinking you can outsmart the beast, you say: “Goofy, do you want a dog bone?” Within nanoseconds, Goofy is at your side, drooling helplessly as you dig a dog bone out of the bin. The next day, Goofy is once again bored and hungry and looks expectantly at you for a treat. But alas, you’re too busy pounding out text messages on your iPhone. Then Goofy gets an idea — when it comes to food, he’s shrewd — and repeats yesterday’s transgression. The plot replays like groundhog day.  Congratulations! You’ve just trained Goofy to jump on the couch whenever he wants a dog bone, which is, like, all the time. This is of course a case of incentivizing the wrong behavior. And business leaders make this same mistake at least as often as dog owners. Why? There tends to be a couple of reasons: 1. Unintended consequences of well intentioned but misguided incentives The first explanation is the most benign. In these cases, managers simply fail to think through the logical consequence of their directives. In retrospect, you may think some of these examples are ludicrous knowing in advance that I’m highlighting incentives that backfired, but I can assure you that each of these situations draws on real world examples — and there are plenty more to choose from.

2. Disingenuous unwillingness to incentivize allegedly desired behaviors Dogs learn early on to watch what their owners do, not what they say. They are after all, dogs. A common example of this same phenomenon in business is when executives disingenuously say the politically correct thing about their priorities but blatantly and knowingly incentivize contrary behaviors. Examples abound.

When there is a clear disconnect between stated objectives and incentivized behavior, institutions lose credibility and authenticity in the eyes of their customers and employees. ******************************************** As I put the finishing touches on this blog entry, my Labrador Retriever is besides me, where else, but on the couch. My protestations not withstanding, I lost credibility a long time ago on canine couch rights with my misguided incentives. In their excellent Harvard Business Review article aptly titled “Big-Bang Disruption”, Paul Nunes and Larry Downes make the case that disruptive new entrants will radically transform more industries far faster than originally envisioned by Clay Christensen in his landmark treatise on this subject 18 years ago. The authors attribute the accelerating pace and scope of disruption to:

With respect to how the new generation of disruptors are likely to impact incumbent market leaders, Nunes and Downes warn: “You can’t see big-bang disruption coming. You can’t stop it. You can’t overcome it. Old-style disruption posed the innovator’s dilemma. Big-bang disruption is the innovator’s disaster. And it will be keeping executives in every industry in a cold sweat for a long time to come.” If you accept this premise (as I do), it leads inexorably to the question every company should be asking themselves: are we innovative enough to be the disruptor and not the disruptee in the next wave of transformational change in our industry? While there are a number of diagnosticsdesigned to test whether companies have a culture conducive to promote innovation, there is one salient indicator that warrants particular attention: how does your company deal with “truth-tellers”? Nunes and Downes define truth tellers as “internal or external seers who can predict the future with insight and clarity. In every industry there are a handful of these visionaries, whose talents are based on equal parts genius and complete immersion in the industry’s inner workings. They may be employees far below the ranks of senior management, working on the front lines of competition and change. They may not be your employees at all. Longtime customers, venture capitalists, industry analysts, and science fiction writers may all be truth tellers.”  Truth tellers play a particularly important role in presaging the need and opportunity to develop new business models which disrupt incumbent business positions, long before the need to change becomes obvious (by which time it’s often too late to stop the destruction of your business by a disruptive newcomer). By their nature, truth-tellers make most business leaders uncomfortable:

Sadly, over a long career in senior management consulting, I’ve witnessed far too many cases where executives not only fail to continuously seek the counsel of truth-tellers, but rather willfully prevent such voices from being heard and evaluated within the organization. What are some of the mechanisms executives use to stifle truth teller input?:

The New York Times carried an ominous story this week on the souring outlook for Barnes & Noble’s Nook business, portending perhaps its exit from the e-reader and tablet markets. The Nook’s decline comes despite its technical competence and the recent infusion of $600 million of capital by Microsoft. As the Times notes, “going into the 2012 Christmas season, the Nook HD, Barnes & Noble’s entrant into the 7-inch and 9-inch tablet market, was winning rave reviews from technology critics who praised its high-quality screen. Editors at CNET called it “a fantastic tablet value” and David Pogue in The New York Times told readers choosing between the Nook HD and Kindle Fire that the Nook “is the one to get.” Unfortunately, high marks from pundits didn’t translate into sales. Nook sales stalled over the Christmas season, losses mounted and profit and revenue guidance has been reduced. What happened? The Times article shares this explanation: “In many ways it is a great product,” Sarah Rotman Epps, a senior analyst at Forrester, said of the Nook tablet. “It was a failure of brand, not product. The Barnes & Noble brand is just very small.” I beg to differ. The Nook’s problems go far beyond B&N’s brand strength. There are three fundamental reasons for Nook’s failure that have implications for any company (and eventually this means every company) facing technology disruption:

2. Disruption redux More broadly the Nook story is yet another example of how disruptive technologies transform value chains, destroying incumbents who no longer create value in the new industry order. With the advent of e-reading devices and digital publishing, book retailers and publishers are severely threatened. We’ve been to this dance before in the music industry, where incumbent retail leaders were essentially wiped out. For a variety of reasons, bookstores (if not the Nook) are likely to survive for quite some time, but only at a fraction of their former scale.Was B&N’s decline inevitable, given the transition from print to digital books? One could ask the same question of Amazon, whose dominance of book sales on amazon.com was equally threatened by e-reader technology. But to Jeff Bezos’ credit, Amazon chose to disrupt itself by aggressively launching the Kindle business, which quickly established itself as the dominant digital book platform. By the time B&N responded with its own Nook devices and e-bookstore, it was too late.The willingness to disrupt one’s own core business before someone else does it to you is a hallmark of inspired leadership. Bezos rules. 3. Stuff Happens! What’s up with Microsoft? As a play on the well known adage, “Disruption Also Happens”! In every industry, the question isn’t whether but only when. The only way to survive and prosper through successive waves of disruption is to be the disruptor, not the disruptee!One would think Microsoft would have learned this lesson by now. Over the past decade, Microsoft has managed to miss five of the most transformative disruptions in the high tech sector:

Bottom line: Serial innovation is the only proven antidote to the accelerating pace of disruptive technologies. It certainly looks like Barnes & Noble and Microsoft have not been up to the task. In theory, effective business strategy is straightforwardly simple. The building blocks are strategic clarity and alignment:

A sage piece of investment advice is relevant in answering this question for established businesses. It has been suggested that when deciding whether to hold or sell a stock, it's useful to ask oneself: "would I buy the stock now if I didn't own it?" If the answer is yes, hold. If no, sell. What guidance does this advice provide to business managers about strategy? In a similar vein, managers should periodically ask themselves two questions:

But in fact, most companies trapped with outdated products and/or organizational capabilities fight to defend their losing hand, with predictably poor results. In short, too many executives are guilty of strategic inertia. Take the book publishing industry for example. Long after the Amazon Kindle had launched, when it was inescapably obvious that ebooks were going to be a major force in the industry, book publishing CEO's should have been asking themselves what new skills they needed to cultivate in their organizations and what new, enhanced products they needed to succeed in the post-digital industry. Instead, too many publishing execs took out their frustration with the growth of ebooks -- which they viewed as threatening their value proposition and price realization -- on consumers! How? First by selectively delaying the release of popular frontlist books in digital form and then engaging in a nasty, allegedly collusive price fixing fight with Amazon to impose a significant increase in ebook consumer prices. Early adopters of ebooks were amongst the most avid readers in the country -- the very customers book publishers should most want to serve. And yet, one Big Six publishing CEO, commenting on her company's decision to start delaying the release of best sellers in ebook form (which had been standard industry practice at the time) noted: "with new electronic readers coming and sales booming, we need to do this now, before the installed base of ebook reading devices gets to a size where doing it would be impossible." Unless your company is committed to continuously update your capabilities to deliver what consumers value, your strategy will not succeed in the long term. The proof that this is easier said than done is that so few companies succeed in sustaining long term profitable gro In my last blog post, I noted the importance of strategic clarity, in terms of the ability of your company to articulate who you are selling to; what is the value proposition and how you can achieve competitive advantage in delivering designated products and services.

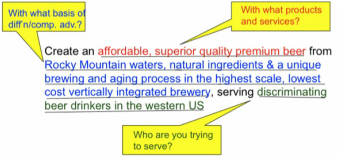

Easier said than done! But let's stipulate that your company has crystallized its strategy in these terms. The next step is to ensure you can capture the inherent value in your strategy through strategic alignment. Simply stated, strategic alignment is the development of a company's capabilities -- it's processes, operations, management systems and culture -- to uniquely support its strategy and desired value proposition. Here are a couple examples to break through the jargon. What do Southwest Airlines and BMW have in common? Very little actually, starting with distinctly different strategic priorities and value propositions. Southwest strives to deliver frequent, friendly reliable flights to price-sensitive leisure and business travelers at a cost others can't profitably match. BMW, on the other hand strives to deliver "ultimate driving machines" at a premium price that delivers value to a select segment of automotive enthusiasts. Each of these value propositions can be highly successful, but only if these companies align their core competencies to consistently, efficiently and effectively execute their chosen strategy. In Southwest's case, this entails highly standardized and simplified flight operations (e.g. one plane type, one class of service, no meals), industry leading labor relations to foster a service-oriented culture and highly disciplined management to avoid over-extending route coverage in this highly cyclical industry. The net result has been decades of extraordinary shareholder value growth, with no morale-killing layoffs in an industry where most legacy airline competitors have been in and (sometimes) out of bankruptcy. BMW on the other hand needs very different core competencies to support its distinctive strategic mission -- namely an organization that emphasizes R&D, state-of-the-art engineering and product development processes and a culture that encourages a commitment to best-in-class products. These are expensive capabilities to develop and maintain, but the company is explicitly investing to deliver value to a class of customer that is able and willing to pay a premium for consistently superior products. Companies that succeed in creating a tight linkage between their strategic intent and aligned capabilities are very difficult for competitors to copy. Sure, it’s easy for an airline competitor to temporarily slash fares to match Southwest, but unless they have the same underlying operational focus, organizational culture and management discipline, their cost structures will not allow a permanent low-fare position. Similarly, automotive competitors have run ads for years suggesting their products compare favorably with BMW (at a far lower price). But the marketplace has generally continued to recognize and reward BMW’s product excellence, despite its premium prices. In sound bite terms, it seems so simple: clearly articulate your strategy (who/what/how) and align all your capabilities to support superior execution. In my next post, I’ll opine on why so many companies struggle to meet these two strategic imperatives.  One of the early topics covered in my business strategy course at Columbia Business School is the importance of strategic clarity. Simply stated, the principle is that a prerequisite for sustained success is the ability of a company to clearly state its business strategy in terms of three defining building blocks:

It sounds simple doesn't it? Most of my MBA students think so.... until we put the principle to a test. An excellent Harvard Business Review article on this topic entitled Can You Say What Your Strategy Is challenges companies to articulate their strategy in terms of the elements above in 35 words or less. Why reduce strategic intent to a tweet? Because it stress tests whether your company truly does have strategic clarity that can be easily understood (and hopefully embraced) by your shareholders, employees and customers. In our class, students are asked to articulate the business strategy of the Coors beer company in the 1970's and contrast it to the company's apparent strategy today. What emerges is that:

For what it's worth, here's the school solution on Coors' mid-1970s strategy in 35 words (minus the financial objective, which wasn't disclosed in the case study reading): While obviously, even the most well conceived statement of business strategy still needs to be effectively executed, strategic clarity is a prerequisite to success. To demonstrate the relevance of strategic clarity, try this at home: think of the the three best and least well managed companies that first come to your mind. Now ask yourself, which group of companies appears to have a clearer, more "tweetable" business strategy? How about your company? Can you tweet the essence of your business strategy that makes a compelling case for how and why you will win in the marketplace? |

Len ShermanAfter 40 years in management consulting and venture capital, I joined the faculty of Columbia Business School, teaching courses in business strategy and corporate entrepreneurship Categories

All

Archives by title

How MIT Dragged Uber Through Public Relations Hell Is Softbank Uber's Savior? Why Can't Uber Make Money? Looking For Growth In All The Wrong Places Three Management Ideas That Need to Die Wells Fargo and the Lobster In the Pot Jumping to the Wrong Conclusions on the AT&T/Time Warner Merger What Kind Of Products Are You Really Selling? What Shakespeare Thinks About Brian Williams Are Customer-Friendly CEO’s Bad for Business? Uncharted Waters: What to Make Of Amazon’s Chronic Lack of Profits What Happens When David Becomes Goliath…Are Large Corporations Destined To Fail? Advice to Publishers: Don’t Fight For Your Honor, Fight For Your Lives! Amazon should be viewed as a fierce competitor in its dispute with publisher Hachette Men (And Women) Behaving Badly Why some brands “just don’t get no respect!” Courage and Faustian Bargains Sun Tzu and the Art of Disrupting Higher Education Nobody Cares What You Think! Product Complexity: Less Can Be More Apple's Product Strategy: No News Is Good News Willful Suspension of Belief In The Book Publishing Industry Whither Higher Education Timing Is Everything Teachable Moments -- The Curious Case of JC Penney What Dogs Can Teach Us About Business Are You Ready For Big-Bang Disruption? When Being Good Isn’t Good Enough Is Apple Losing Its Mojo? Blowing Up Old Habits What Is Apple's Product Strategy--Strategic Rigidity or Enlightened Expansion Strategic Inertia Strategic Alignment Strategic Clarity Archives by date

March 2018

|

RSS Feed

RSS Feed