|

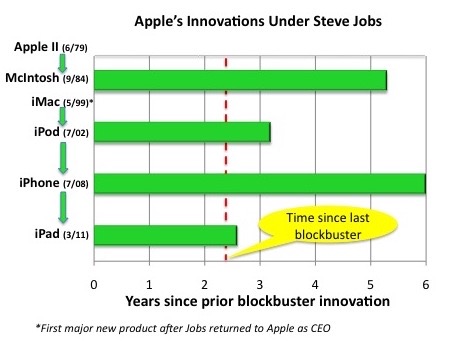

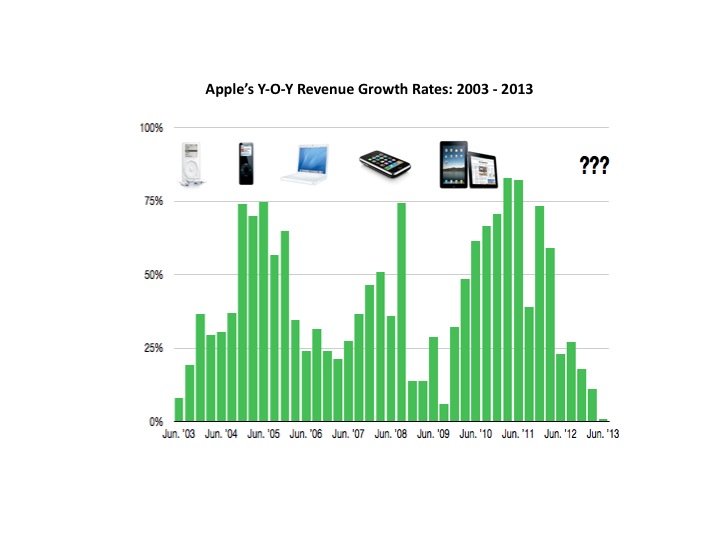

Question: how long should it take for a company to come up with an industry-changing, category-redefining, market-dominating new technology with sales of $10 billion or more. Answer: For the vast majority of companies, the answer of course is never. For Apple, the answer appears to be, not soon enough. It has been 2.3 years since Apple’s last game-changer — the iPad, which helped drive year-on-year profitable sales growth of 30+% (and mostly >50%) for ten consecutive quarters. During this astonishing run, Apple’s annual revenues climbed over $100 billion and its stock peaked at >$700 per share. But predictably — in fact inevitably — Apple’s growth rate has since slowed, and nervous investors have driven its share price down by 45% from peak. To add insult to injury, numerous pundits have declared that Apple’s uncanny knack for innovation died with Steve Jobs’ passing and its best days are clearly behind it. To be honest, it does feel like a long time since Apple launched a home run product, and it’s easy to believe that if Steve Jobs were still around, we wouldn’t still be waiting for some new form of technical wizardry. But a closer look at Jobs’ legacy for serial innovation suggests that such expectations are unreasonable. As noted in the exhibit below, during his two CEO stints at Apple, Steve Jobs never launched consecutive blockbusters in less than 2.3 years. In fact, it took six years for Apple to pivot from the iPod to the iPhone. From Apple II to the MacIntosh took 5.3 years. And even though Apple was working hard on tablets long before the launch of its smartphone, the iPad was launched 2.6 years after the iPhone.  So why is Tim Cook being held to an unprecedentedly higher standard for product innovation? Perhaps because investors have been spooked by the sharp declines in Apple’s growth rates of late. But as shown below, Apple has always ridden a revenue growth roller coaster between game changing product launches.  At least for now, what we’re seeing or not seeing from Apple is nothing new. The company’s future — as it always has been — will be determined by whether it can pull off yet another new product game-changer. Pundits and investors can have legitimately differing opinions on this question, but it is clearly too early to declare that Apple’s inability to launch blockbuster products over the past 2+ years somehow proves that innovation is dead at the company.

So what’s behind the title of this piece — that for Apple, no news is actually good news? There actually were two shreds of reassurance coming out of Apple’s otherwise mostly inconsequential quarterly earnings report this week. First, Apple announced surprisingly strong iPhone sales, exceeding analyst estimates for the quarter by 20%. That iPhone sales remained strong despite Samsung’s recent Galaxy S4 launch, supported by a breathtakingly lavish advertising budget, reaffirms just how strong the now venerable iPhone design really was. How large is “breathtaking”? Samsung’s global marketing expenditures for mobile devices is estimated to currently be on an annual run rate of $12 billion, more than the advertising spend by Apple, HP, Dell, Microsoft, and Coca Cola combined on all their products!. In that context, Apple’s market resilience is notable. Second, and more importantly, Tim Cook’s commentary during this week’s analyst meeting reaffirmed that the company has not abandoned Steve Jobs’ “outside-in” strategic perspective, which focuses the company’s energies on creating great products and customer experiences. In response to an analyst question on whether internal growth targets drive Apple’s product development and launch timing, Tim Cook responded: “The way I think about is, we’re here to make great products and we think that if we focus on that and do that really, really well that the financial metrics will also come… If you don’t start at that level you can wind up creating things that people don’t want.” While obviously, it would have been beneficial for Apple to have launched yet another blockbuster product by now in what would have been an unprecedentedly short amount of time, Apple’s greatest threat would be rushing to market with unimaginative products that tarnish its stellar reputation for product excellence. No one, starting with Tim Cook himself, claims he’s another Steve Jobs. But give the current CEO credit: he gets it. He is committed to sustaining Apple’s legacy for product excellence. Cook deserves at least as much time as his predecessor to tell if he can deliver.

0 Comments

The New York Times Editorial Board’s opinion on the recent e-book pricing court decision echoes the publishing industry’s longstanding position: “The big picture is that while Apple’s pact with the publishers raised prices in the short term, it also brought much-needed competition to the e-book marketplace. It is estimated that Apple now controls 10 percent of that market and Amazon 65 percent, with Barnes & Noble and others splitting the rest. That is healthier for the publishers and for consumers, too.” Underscoring the Times’ argument is a widely held, visceral conviction amongst publishers that Amazon’s growing share of the market for both paper and digital books has been bad for the industry, for consumers and even for society as a whole, given the hallowed role of the written word in our lives. However passionately held these beliefs are, they ultimately were deemed to hold little legal merit, as U.S. District Court Judge Denise Cote ruled decisively against Apple in the antitrust case — and by extension, against the publishers who had already settled to avoid mounting legal costs. While the penalty ruling has yet to be rendered, Judge Cote left no doubt that this case was not even a close call in her blistering 160 page opinion. “Apple and the Publisher Defendants shared one overarching interest that there be no price competition at the retail level. Apple did not want to compete with Amazon (or any other e-book retailer) on price; and the Publisher Defendants wanted to end Amazon’s $9.99 pricing and increase significantly the prevailing price point for e-books. With a full appreciation of each other’s interests, Apple and the Publisher Defendants agreed to work together to eliminate retail price competition in the e-book market and raise the price of e-books above $9.99.” While throughout this legal dispute, book publishers portrayed themselves as endangered curators of great literary work, what lies at the core of this case is the frightening reality that digital disruption of the book industry leaves publishers in a highly vulnerable and uncertain position. Even had Apple won this case on the publishers’ behalf (or prevails in its promised appeal), publishers will still need to figure out how to continue to add value in an environment where they no longer serve as the predominant gatekeeper, deciding which books get published, promoted and retailed to consumers. This is a legitimately scary concern, as exemplified by prior victims of technology-driven disintermediation, including Kodak, Blockbuster and Tower Records. So it is understandable that book publishers would seek legal relief from the inexorable erosion of their competitive position. But the ruling in this case was correct, in that accepting the position advocated by Apple, book publishers and the New York Times would require the willful suspension of belief in the intent of antitrust law and in the realities of free market competition as noted below:

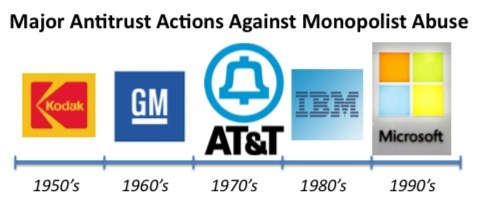

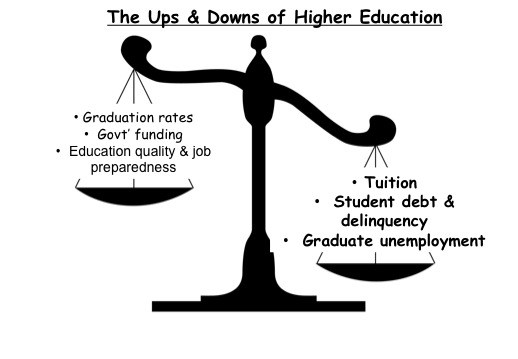

In the end, this anti-trust trial proved to be a slam-dunk case. The DOJ’s claims were backed up by damaging e-mails and phone logs establishing Apple’s and the publishers’ anti-competitive intent and by data that showed the incontrovertibly harmful consumer impact of their collusive behavior. The issue for Apple and publishers of course was never an overriding concern with what was best for consumers, but only what was best for them. This isn’t unusually callous behavior… it’s just business. Apple did not want to compete head on with Amazon in the retail market, and conspired with publishers who feared that Amazon would eventually demand lower wholesale prices, starting with e-books and eventually expanding to all books. To publishers, Amazon posed an existential threat. But the notion that publishers need to be exempted from broadly applicable antitrust constraints on collusive behavior to protect the status quo from the inevitable consequences of digital disruption, is an intellectually tenuous argument at best. The sad fact is that many aspiring authors would argue that the publishing industry has been retreating from its historically laudable role of promoting great literature and important non-fiction work long before the recent explosive growth in e-books. In this view, major publishing houses have generally made life harder for new and mid-list authors by collectively skewing their advances and marketing budgets towards blockbuster titles, often of dubious literary distinction. The logical corollary to this view is that the possibility of self-publishing e-books has opened more opportunities for more authors to get to market, giving more choice to consumers at lower prices. Some hard working, earnest (and often poorly paid) managers in the book publishing industry will undoubtedly take strong exception to this view of their noble profession and deeply believe that antitrust action -- if any — should have been brought against the monopolist evil empire in Seattle. But in the end, it is the marketplace and not the courts that will dictate the outcome of “the new normal” in the book publishing industry. If you have any doubt that even seemingly indomitable monopolists are not exempt from the need for continuous innovation and adaptive change with or without judicial restraint, consider the following. Each of the companies depicted below were accused at the height of their market power of monopolistic, antitrust behavior. Yet none of these companies were able to continue to dominate the industries in which they once held market shares of ~50% – 90+%. In the decades following government charges of antitrust abuses (some won, most lost), Kodak and GM went bankrupt, what was left of AT&T was sold off at a fire-sale price and IBM and Microsoft are no longer considered monopolist threats.  More recently, Apple’s iTunes, which once looked invincible in the music download music business is now facing stiff competition from a number of streaming music providers, including Pandora, Spotify, Songza, Google and yes, even Amazon! So in the book industry, as in every other industry, every player — including Amazon — will have to continue to adapt their business models to deliver value in an industry subject to relentless change. Transient competitive advantages will come and go, but business outcomes will be ultimately be determined in the marketplace, not in the courts. By now, you have undoubtedly seen press coverage on “the crisis” in higher education, signified by disturbing trends in a number of performance indicators depicted below.  What adds urgency to the purported crisis (which in fact has been brewing for decades) is a gnawing concern that the US is losing its historical higher education leadership — particularly in STEM disciplines — to China, India and other emerging powers. On a brighter note, many observers point to the emergence of Massive Open Online Courses (MOOCs) as the savior that will disrupt and dramatically improve higher education. Some suggest MOOCs will supplant expensive, ineffective classroom education with a cornucopia of web-based offerings taught by the world’s best professors from the best schools on their best day — all for free! Yet, while few would argue with the need for colleges and universities to bend their cost curve, improve accessibility and achieve better education outcomes, the notion that MOOCs will largely replace classroom education in meeting these objectives is naive folly. There is a role for online and on-campus education, and the challenge and opportunity for higher education institutions is to find the optimal mix for their targeted student market. So what can we expect to see in the higher education landscape over the coming decade? For starters, let’s stipulate that the status quo in higher education is unsustainable. No sector of the economy can continue to absorb an ever-higher proportion of household disposable income, particularly with mounting evidence that the quality of higher education outcomes is static at best, and by some measures, actually declining. Defenders of the status quo may point to the fact that despite tuition inflation, a college education remains a good investment relative to non-college attendance. But as Clay Shirky bitingly points out, this argument casts students as hostages in an extortion scheme: “pay us or you’ll be even worse off!” The question of course shouldn’t be whether a college degree provides an adequate (albeit recently declining) return on tuition investment relative to an obviously inadequate alternative, but rather, how can we improve the ROI and accessibility of higher education? There are already signs that market forces are correcting what has traditionally been a hidebound sector of the economy.

But before accepting the dogma that these are early signs of a disruptive tsunami crashing on the shores of college campuses, it is wise to take some cautionary note of impediments to the speed and breadth of disruptive change in higher ed:

To get the discussion rolling, I started by sharing some recent data from widely watched MBA school rankings (Business Week and The Economist) indicating declining student satisfaction with the quality of the MBA education at Columbia and other schools. The intent was to serve as a backdrop to soliciting student suggestions for improvement in business school education. One of the students seemed visibly uncomfortable with where this discussion seemed to be going, and shared a point of view that the CBS community has an obligation to support the school and protect its reputation. In fact, some students amplified this sentiment by noting that any student who gave less than top ratings on published surveys of student satisfaction were hurting themselves and classmates. Recognizing the sensitivity of this topic to those still in the anxious hunt for a post-MBA job, I suggested that for the remainder of the class discussion, students should imagine that a decade has passed, everyone has a great job and we are now merely reflecting back on what might improve MBA education for the next generation of aspiring business leaders, including the possibility of disruptive new formats. To my surprise, one of the students opined that he would still be reluctant to publicly acknowledge concerns with his alma mater for fear that it might weaken his executive stature. In his words, “as long as I have Columbia Business School on my resumé, I’d like it be considered a top-notch B-School. And I hope to play a valued role in recruiting the next generation MBAs from Columbia.” To take this discussion thread one final step, I asked the class at what point their allegiance might shift from supporting their alma mater to supporting the best business interests of their employer, if in fact, a potential conflict emerged. “Suppose,” I hypothesized, “an HR director came to you in your capacity of business unit general manager to report that your company was experiencing excellent results by hiring applicants who had supplemented their undergraduate degree with directly relevant skills via targeted MOOC courses. Starting salaries for this new breed of employee was roughly half the rate of a freshly minted MBA. As a result, she suggested that your company should reduce its historical emphasis on MBA hiring. Would you be receptive to such a suggestion?” One student continued to express discomfort with such a suggestion, thereby providing an unexpected teachable moment regarding just how resistant current stakeholders can be to disruptive threats to the status quo — in educational institutions or corporate entities.  With that caution in mind, what changes in higher education can we expect to see in the years ahead? First of all, let’s return to what I stipulated earlier: despite earlier flame-outs, this time isdifferent and higher education will be disrupted as new technologies enable viable alternatives to the unsustainably high costs and declining value of traditional higher education formats. In the long term, resistance from incumbent stakeholders will eventually be overcome by two large and powerful constituencies poorly served by today’s status quo: the 70% of US adults who do not have a college degree and the large number of employers challenged by a skills gap in the recruiting marketplace. The economic potential that can be unlocked by better serving these large constituencies will continue to attract investment in alternative education delivery models from both the private and public sector. And make no mistake about it: if employers begin to experience positive results in hiring employees who have acquired superior job skills at lower cost than by attending conventional colleges (and therefore may accept lower initial compensation), interest in conventional forms of higher education will decline from both students and employers alike. But these are still early days in the disruption of an extremely large and complex segment of the economy and anyone who tells you they know how it will all sort out — or even worse, cling to simplistic notions such as “MOOCs will largely replace college classrooms” — is either misinformed or naive. There are appropriate roles for both online and on-campus education delivery models, and the challenge is ultimately to find the right balance to improve effectiveness at lower cost. Institutions like Columbia University, who currently has the dubious distinction of charging the highest gross college tuition in the US can in fact continue to provide a superior higher education experience (and justify its inherently higher costs), but only by addressing two questions I believe every university president should currently be asking themselves:

Obviously a high level of personalization is not possible in MOOCs with tens of thousands of students. So if universities want to remain leaders in delivering the best quality higher education, they have to ensure they provide more student access to the best teachers backed by research and relevant experience, who are incentivized and motivated to spend time interacting meaningfully and individually with their students. Unfortunately, this key differentiator for on-campus education is often not a faculty priority, given the incentives typically in place at research-centric higher ed institutions. In fact, at universities like Columbia or my alma mater MIT, the incentives in place for tenure track faculty are skewed so that the marginal utility of spending an extra hour on research greatly exceeds the marginal utility of an incremental hour devoted to curriculum enhancements, teaching and student interaction. Relatedly, it is already far too common for student TA’s to grade their peers’ homework assignments because professors are unwilling to put in the effort required to provide personalized feedback, or classes have become too large to make such personalization feasible, or both. On the other hand, professors who volunteer to create MOOC courses are likely to be predominantly motivated by teaching excellence and extending their intellectual reach. The best online teachers will attract the most enrollments and the highest student satisfaction ratings. Over time, I fully expect that MOOC platforms will evolve towards revenue-generating business models, precipitating a shift in the balance of power from universities to individual academics and practitioners who develop a global reputation for teaching excellence. If the best teaching professionals increasingly find their best opportunities for global impact and remuneration lie outside traditional higher ed institutions, it may further hollow out the educational excellence of Tier 1 universities. The point here is it that every academic leader should reexamine what it will take to sustain leadership in delivering the highest quality on-campus higher education in the future — not just with respect to traditional delivery models and current protocols, but also against evolving highly disruptive new technologies. The context and priorities will vary from one institution to another. For example, community colleges may choose to focus on online enhancements to classroom education aimed at lowering cost, expanding student coaching (to combat high dropout rates) and enhance flexibility. On the other hand, Tier 1 universities may push the envelope on hybrid teaching models which free up faculty time for more intensive and personalized student interaction. In any event, the question isn’t whether but how higher education institutions catch the wave of disruptive change. With respect to the second key question facing university presidents – whether and how to participate in emerging online learning opportunities – no one can claim to know the precise pace and form that disruptive learning technologies will take over the next decade. But I would argue that it is precisely because of this inherent uncertainty that the appropriate response to early stage disruptive threats (and opportunities) should be extensive low-cost iterative experimentation. Universities need to discover for themselves how to best incorporate new technologies into their on-campus and extended learning environments. I would like to see more higher education institutions aggressively undertaking and sharing experiences from multiple digital learning experiments, including video lectures to “flip” classrooms, MOOC courses to extend learning reach and to gain familiarity with online pedagogical techniques, greater use of video technologies to beam global thought leaders into our classrooms, and experiments with different forms of automated grading for larger online and classroom audiences. What’s holding universities back? The obvious culprits are common to corporate environments as well: budget constraints, misaligned incentives and the ever present FUD. But another barrier is the significant faculty skills gap that constrains many colleges and universities from gaining widespread buy-in to exploit emerging technologies. As a case in point, consider how leading graduate schools have adapted their curricula to train aspiring journalists. Ten years ago, J-School curricula focused predominantly on the tools and techniques for becoming an effective print media reporter. Today, J-School courses emphasize multi-media technologies, social networking and digital photography/editing skills which reflect the radical shifts in reporter roles and news delivery formats. In contrast, graduate students pursuing a career in academia typically get limited formal guidance on general teaching skills, let alone tutorials on emerging technologies to digitally enhance their classrooms. On most campuses, there is simply too little opportunity and incentive for junior or senior faculty to lead the charge on pedagogical experimentation. So for now at least, as is often the case in the corporate sector — Kodak and Blockbuster are exemplars that come to mind — the leading edge of disruptive change is primarily being driven by newcomers rather than incumbent leaders. While it is difficult to predict exactly how new technologies, pedagogies and business models will play out over the coming decade, it is a safe bet that those institutions who stubbornly cling to the status quo are likely to find (painfully) that this time it is real: higher education is in the midst of disruptive, transformative change. |

Len ShermanAfter 40 years in management consulting and venture capital, I joined the faculty of Columbia Business School, teaching courses in business strategy and corporate entrepreneurship Categories

All

Archives by title

How MIT Dragged Uber Through Public Relations Hell Is Softbank Uber's Savior? Why Can't Uber Make Money? Looking For Growth In All The Wrong Places Three Management Ideas That Need to Die Wells Fargo and the Lobster In the Pot Jumping to the Wrong Conclusions on the AT&T/Time Warner Merger What Kind Of Products Are You Really Selling? What Shakespeare Thinks About Brian Williams Are Customer-Friendly CEO’s Bad for Business? Uncharted Waters: What to Make Of Amazon’s Chronic Lack of Profits What Happens When David Becomes Goliath…Are Large Corporations Destined To Fail? Advice to Publishers: Don’t Fight For Your Honor, Fight For Your Lives! Amazon should be viewed as a fierce competitor in its dispute with publisher Hachette Men (And Women) Behaving Badly Why some brands “just don’t get no respect!” Courage and Faustian Bargains Sun Tzu and the Art of Disrupting Higher Education Nobody Cares What You Think! Product Complexity: Less Can Be More Apple's Product Strategy: No News Is Good News Willful Suspension of Belief In The Book Publishing Industry Whither Higher Education Timing Is Everything Teachable Moments -- The Curious Case of JC Penney What Dogs Can Teach Us About Business Are You Ready For Big-Bang Disruption? When Being Good Isn’t Good Enough Is Apple Losing Its Mojo? Blowing Up Old Habits What Is Apple's Product Strategy--Strategic Rigidity or Enlightened Expansion Strategic Inertia Strategic Alignment Strategic Clarity Archives by date

March 2018

|

RSS Feed

RSS Feed