|

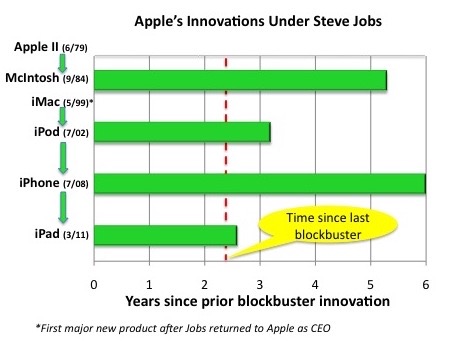

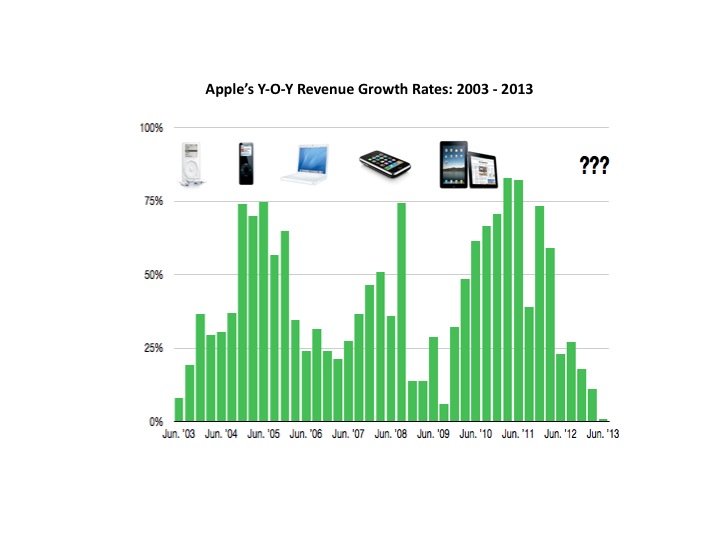

Question: how long should it take for a company to come up with an industry-changing, category-redefining, market-dominating new technology with sales of $10 billion or more. Answer: For the vast majority of companies, the answer of course is never. For Apple, the answer appears to be, not soon enough. It has been 2.3 years since Apple’s last game-changer — the iPad, which helped drive year-on-year profitable sales growth of 30+% (and mostly >50%) for ten consecutive quarters. During this astonishing run, Apple’s annual revenues climbed over $100 billion and its stock peaked at >$700 per share. But predictably — in fact inevitably — Apple’s growth rate has since slowed, and nervous investors have driven its share price down by 45% from peak. To add insult to injury, numerous pundits have declared that Apple’s uncanny knack for innovation died with Steve Jobs’ passing and its best days are clearly behind it. To be honest, it does feel like a long time since Apple launched a home run product, and it’s easy to believe that if Steve Jobs were still around, we wouldn’t still be waiting for some new form of technical wizardry. But a closer look at Jobs’ legacy for serial innovation suggests that such expectations are unreasonable. As noted in the exhibit below, during his two CEO stints at Apple, Steve Jobs never launched consecutive blockbusters in less than 2.3 years. In fact, it took six years for Apple to pivot from the iPod to the iPhone. From Apple II to the MacIntosh took 5.3 years. And even though Apple was working hard on tablets long before the launch of its smartphone, the iPad was launched 2.6 years after the iPhone.  So why is Tim Cook being held to an unprecedentedly higher standard for product innovation? Perhaps because investors have been spooked by the sharp declines in Apple’s growth rates of late. But as shown below, Apple has always ridden a revenue growth roller coaster between game changing product launches.  At least for now, what we’re seeing or not seeing from Apple is nothing new. The company’s future — as it always has been — will be determined by whether it can pull off yet another new product game-changer. Pundits and investors can have legitimately differing opinions on this question, but it is clearly too early to declare that Apple’s inability to launch blockbuster products over the past 2+ years somehow proves that innovation is dead at the company.

So what’s behind the title of this piece — that for Apple, no news is actually good news? There actually were two shreds of reassurance coming out of Apple’s otherwise mostly inconsequential quarterly earnings report this week. First, Apple announced surprisingly strong iPhone sales, exceeding analyst estimates for the quarter by 20%. That iPhone sales remained strong despite Samsung’s recent Galaxy S4 launch, supported by a breathtakingly lavish advertising budget, reaffirms just how strong the now venerable iPhone design really was. How large is “breathtaking”? Samsung’s global marketing expenditures for mobile devices is estimated to currently be on an annual run rate of $12 billion, more than the advertising spend by Apple, HP, Dell, Microsoft, and Coca Cola combined on all their products!. In that context, Apple’s market resilience is notable. Second, and more importantly, Tim Cook’s commentary during this week’s analyst meeting reaffirmed that the company has not abandoned Steve Jobs’ “outside-in” strategic perspective, which focuses the company’s energies on creating great products and customer experiences. In response to an analyst question on whether internal growth targets drive Apple’s product development and launch timing, Tim Cook responded: “The way I think about is, we’re here to make great products and we think that if we focus on that and do that really, really well that the financial metrics will also come… If you don’t start at that level you can wind up creating things that people don’t want.” While obviously, it would have been beneficial for Apple to have launched yet another blockbuster product by now in what would have been an unprecedentedly short amount of time, Apple’s greatest threat would be rushing to market with unimaginative products that tarnish its stellar reputation for product excellence. No one, starting with Tim Cook himself, claims he’s another Steve Jobs. But give the current CEO credit: he gets it. He is committed to sustaining Apple’s legacy for product excellence. Cook deserves at least as much time as his predecessor to tell if he can deliver.

0 Comments

The New York Times Editorial Board’s opinion on the recent e-book pricing court decision echoes the publishing industry’s longstanding position: “The big picture is that while Apple’s pact with the publishers raised prices in the short term, it also brought much-needed competition to the e-book marketplace. It is estimated that Apple now controls 10 percent of that market and Amazon 65 percent, with Barnes & Noble and others splitting the rest. That is healthier for the publishers and for consumers, too.” Underscoring the Times’ argument is a widely held, visceral conviction amongst publishers that Amazon’s growing share of the market for both paper and digital books has been bad for the industry, for consumers and even for society as a whole, given the hallowed role of the written word in our lives. However passionately held these beliefs are, they ultimately were deemed to hold little legal merit, as U.S. District Court Judge Denise Cote ruled decisively against Apple in the antitrust case — and by extension, against the publishers who had already settled to avoid mounting legal costs. While the penalty ruling has yet to be rendered, Judge Cote left no doubt that this case was not even a close call in her blistering 160 page opinion. “Apple and the Publisher Defendants shared one overarching interest that there be no price competition at the retail level. Apple did not want to compete with Amazon (or any other e-book retailer) on price; and the Publisher Defendants wanted to end Amazon’s $9.99 pricing and increase significantly the prevailing price point for e-books. With a full appreciation of each other’s interests, Apple and the Publisher Defendants agreed to work together to eliminate retail price competition in the e-book market and raise the price of e-books above $9.99.” While throughout this legal dispute, book publishers portrayed themselves as endangered curators of great literary work, what lies at the core of this case is the frightening reality that digital disruption of the book industry leaves publishers in a highly vulnerable and uncertain position. Even had Apple won this case on the publishers’ behalf (or prevails in its promised appeal), publishers will still need to figure out how to continue to add value in an environment where they no longer serve as the predominant gatekeeper, deciding which books get published, promoted and retailed to consumers. This is a legitimately scary concern, as exemplified by prior victims of technology-driven disintermediation, including Kodak, Blockbuster and Tower Records. So it is understandable that book publishers would seek legal relief from the inexorable erosion of their competitive position. But the ruling in this case was correct, in that accepting the position advocated by Apple, book publishers and the New York Times would require the willful suspension of belief in the intent of antitrust law and in the realities of free market competition as noted below:

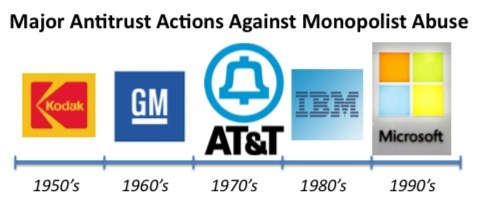

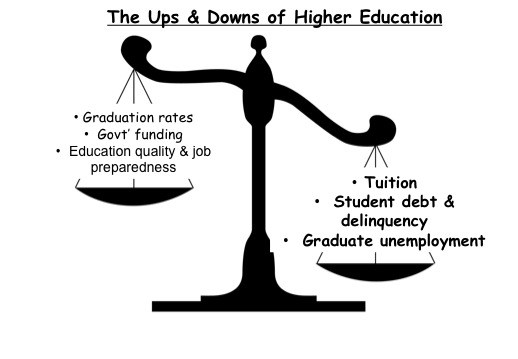

In the end, this anti-trust trial proved to be a slam-dunk case. The DOJ’s claims were backed up by damaging e-mails and phone logs establishing Apple’s and the publishers’ anti-competitive intent and by data that showed the incontrovertibly harmful consumer impact of their collusive behavior. The issue for Apple and publishers of course was never an overriding concern with what was best for consumers, but only what was best for them. This isn’t unusually callous behavior… it’s just business. Apple did not want to compete head on with Amazon in the retail market, and conspired with publishers who feared that Amazon would eventually demand lower wholesale prices, starting with e-books and eventually expanding to all books. To publishers, Amazon posed an existential threat. But the notion that publishers need to be exempted from broadly applicable antitrust constraints on collusive behavior to protect the status quo from the inevitable consequences of digital disruption, is an intellectually tenuous argument at best. The sad fact is that many aspiring authors would argue that the publishing industry has been retreating from its historically laudable role of promoting great literature and important non-fiction work long before the recent explosive growth in e-books. In this view, major publishing houses have generally made life harder for new and mid-list authors by collectively skewing their advances and marketing budgets towards blockbuster titles, often of dubious literary distinction. The logical corollary to this view is that the possibility of self-publishing e-books has opened more opportunities for more authors to get to market, giving more choice to consumers at lower prices. Some hard working, earnest (and often poorly paid) managers in the book publishing industry will undoubtedly take strong exception to this view of their noble profession and deeply believe that antitrust action -- if any — should have been brought against the monopolist evil empire in Seattle. But in the end, it is the marketplace and not the courts that will dictate the outcome of “the new normal” in the book publishing industry. If you have any doubt that even seemingly indomitable monopolists are not exempt from the need for continuous innovation and adaptive change with or without judicial restraint, consider the following. Each of the companies depicted below were accused at the height of their market power of monopolistic, antitrust behavior. Yet none of these companies were able to continue to dominate the industries in which they once held market shares of ~50% – 90+%. In the decades following government charges of antitrust abuses (some won, most lost), Kodak and GM went bankrupt, what was left of AT&T was sold off at a fire-sale price and IBM and Microsoft are no longer considered monopolist threats.  More recently, Apple’s iTunes, which once looked invincible in the music download music business is now facing stiff competition from a number of streaming music providers, including Pandora, Spotify, Songza, Google and yes, even Amazon! So in the book industry, as in every other industry, every player — including Amazon — will have to continue to adapt their business models to deliver value in an industry subject to relentless change. Transient competitive advantages will come and go, but business outcomes will be ultimately be determined in the marketplace, not in the courts. By now, you have undoubtedly seen press coverage on “the crisis” in higher education, signified by disturbing trends in a number of performance indicators depicted below.  What adds urgency to the purported crisis (which in fact has been brewing for decades) is a gnawing concern that the US is losing its historical higher education leadership — particularly in STEM disciplines — to China, India and other emerging powers. On a brighter note, many observers point to the emergence of Massive Open Online Courses (MOOCs) as the savior that will disrupt and dramatically improve higher education. Some suggest MOOCs will supplant expensive, ineffective classroom education with a cornucopia of web-based offerings taught by the world’s best professors from the best schools on their best day — all for free! Yet, while few would argue with the need for colleges and universities to bend their cost curve, improve accessibility and achieve better education outcomes, the notion that MOOCs will largely replace classroom education in meeting these objectives is naive folly. There is a role for online and on-campus education, and the challenge and opportunity for higher education institutions is to find the optimal mix for their targeted student market. So what can we expect to see in the higher education landscape over the coming decade? For starters, let’s stipulate that the status quo in higher education is unsustainable. No sector of the economy can continue to absorb an ever-higher proportion of household disposable income, particularly with mounting evidence that the quality of higher education outcomes is static at best, and by some measures, actually declining. Defenders of the status quo may point to the fact that despite tuition inflation, a college education remains a good investment relative to non-college attendance. But as Clay Shirky bitingly points out, this argument casts students as hostages in an extortion scheme: “pay us or you’ll be even worse off!” The question of course shouldn’t be whether a college degree provides an adequate (albeit recently declining) return on tuition investment relative to an obviously inadequate alternative, but rather, how can we improve the ROI and accessibility of higher education? There are already signs that market forces are correcting what has traditionally been a hidebound sector of the economy.

But before accepting the dogma that these are early signs of a disruptive tsunami crashing on the shores of college campuses, it is wise to take some cautionary note of impediments to the speed and breadth of disruptive change in higher ed:

To get the discussion rolling, I started by sharing some recent data from widely watched MBA school rankings (Business Week and The Economist) indicating declining student satisfaction with the quality of the MBA education at Columbia and other schools. The intent was to serve as a backdrop to soliciting student suggestions for improvement in business school education. One of the students seemed visibly uncomfortable with where this discussion seemed to be going, and shared a point of view that the CBS community has an obligation to support the school and protect its reputation. In fact, some students amplified this sentiment by noting that any student who gave less than top ratings on published surveys of student satisfaction were hurting themselves and classmates. Recognizing the sensitivity of this topic to those still in the anxious hunt for a post-MBA job, I suggested that for the remainder of the class discussion, students should imagine that a decade has passed, everyone has a great job and we are now merely reflecting back on what might improve MBA education for the next generation of aspiring business leaders, including the possibility of disruptive new formats. To my surprise, one of the students opined that he would still be reluctant to publicly acknowledge concerns with his alma mater for fear that it might weaken his executive stature. In his words, “as long as I have Columbia Business School on my resumé, I’d like it be considered a top-notch B-School. And I hope to play a valued role in recruiting the next generation MBAs from Columbia.” To take this discussion thread one final step, I asked the class at what point their allegiance might shift from supporting their alma mater to supporting the best business interests of their employer, if in fact, a potential conflict emerged. “Suppose,” I hypothesized, “an HR director came to you in your capacity of business unit general manager to report that your company was experiencing excellent results by hiring applicants who had supplemented their undergraduate degree with directly relevant skills via targeted MOOC courses. Starting salaries for this new breed of employee was roughly half the rate of a freshly minted MBA. As a result, she suggested that your company should reduce its historical emphasis on MBA hiring. Would you be receptive to such a suggestion?” One student continued to express discomfort with such a suggestion, thereby providing an unexpected teachable moment regarding just how resistant current stakeholders can be to disruptive threats to the status quo — in educational institutions or corporate entities.  With that caution in mind, what changes in higher education can we expect to see in the years ahead? First of all, let’s return to what I stipulated earlier: despite earlier flame-outs, this time isdifferent and higher education will be disrupted as new technologies enable viable alternatives to the unsustainably high costs and declining value of traditional higher education formats. In the long term, resistance from incumbent stakeholders will eventually be overcome by two large and powerful constituencies poorly served by today’s status quo: the 70% of US adults who do not have a college degree and the large number of employers challenged by a skills gap in the recruiting marketplace. The economic potential that can be unlocked by better serving these large constituencies will continue to attract investment in alternative education delivery models from both the private and public sector. And make no mistake about it: if employers begin to experience positive results in hiring employees who have acquired superior job skills at lower cost than by attending conventional colleges (and therefore may accept lower initial compensation), interest in conventional forms of higher education will decline from both students and employers alike. But these are still early days in the disruption of an extremely large and complex segment of the economy and anyone who tells you they know how it will all sort out — or even worse, cling to simplistic notions such as “MOOCs will largely replace college classrooms” — is either misinformed or naive. There are appropriate roles for both online and on-campus education delivery models, and the challenge is ultimately to find the right balance to improve effectiveness at lower cost. Institutions like Columbia University, who currently has the dubious distinction of charging the highest gross college tuition in the US can in fact continue to provide a superior higher education experience (and justify its inherently higher costs), but only by addressing two questions I believe every university president should currently be asking themselves:

Obviously a high level of personalization is not possible in MOOCs with tens of thousands of students. So if universities want to remain leaders in delivering the best quality higher education, they have to ensure they provide more student access to the best teachers backed by research and relevant experience, who are incentivized and motivated to spend time interacting meaningfully and individually with their students. Unfortunately, this key differentiator for on-campus education is often not a faculty priority, given the incentives typically in place at research-centric higher ed institutions. In fact, at universities like Columbia or my alma mater MIT, the incentives in place for tenure track faculty are skewed so that the marginal utility of spending an extra hour on research greatly exceeds the marginal utility of an incremental hour devoted to curriculum enhancements, teaching and student interaction. Relatedly, it is already far too common for student TA’s to grade their peers’ homework assignments because professors are unwilling to put in the effort required to provide personalized feedback, or classes have become too large to make such personalization feasible, or both. On the other hand, professors who volunteer to create MOOC courses are likely to be predominantly motivated by teaching excellence and extending their intellectual reach. The best online teachers will attract the most enrollments and the highest student satisfaction ratings. Over time, I fully expect that MOOC platforms will evolve towards revenue-generating business models, precipitating a shift in the balance of power from universities to individual academics and practitioners who develop a global reputation for teaching excellence. If the best teaching professionals increasingly find their best opportunities for global impact and remuneration lie outside traditional higher ed institutions, it may further hollow out the educational excellence of Tier 1 universities. The point here is it that every academic leader should reexamine what it will take to sustain leadership in delivering the highest quality on-campus higher education in the future — not just with respect to traditional delivery models and current protocols, but also against evolving highly disruptive new technologies. The context and priorities will vary from one institution to another. For example, community colleges may choose to focus on online enhancements to classroom education aimed at lowering cost, expanding student coaching (to combat high dropout rates) and enhance flexibility. On the other hand, Tier 1 universities may push the envelope on hybrid teaching models which free up faculty time for more intensive and personalized student interaction. In any event, the question isn’t whether but how higher education institutions catch the wave of disruptive change. With respect to the second key question facing university presidents – whether and how to participate in emerging online learning opportunities – no one can claim to know the precise pace and form that disruptive learning technologies will take over the next decade. But I would argue that it is precisely because of this inherent uncertainty that the appropriate response to early stage disruptive threats (and opportunities) should be extensive low-cost iterative experimentation. Universities need to discover for themselves how to best incorporate new technologies into their on-campus and extended learning environments. I would like to see more higher education institutions aggressively undertaking and sharing experiences from multiple digital learning experiments, including video lectures to “flip” classrooms, MOOC courses to extend learning reach and to gain familiarity with online pedagogical techniques, greater use of video technologies to beam global thought leaders into our classrooms, and experiments with different forms of automated grading for larger online and classroom audiences. What’s holding universities back? The obvious culprits are common to corporate environments as well: budget constraints, misaligned incentives and the ever present FUD. But another barrier is the significant faculty skills gap that constrains many colleges and universities from gaining widespread buy-in to exploit emerging technologies. As a case in point, consider how leading graduate schools have adapted their curricula to train aspiring journalists. Ten years ago, J-School curricula focused predominantly on the tools and techniques for becoming an effective print media reporter. Today, J-School courses emphasize multi-media technologies, social networking and digital photography/editing skills which reflect the radical shifts in reporter roles and news delivery formats. In contrast, graduate students pursuing a career in academia typically get limited formal guidance on general teaching skills, let alone tutorials on emerging technologies to digitally enhance their classrooms. On most campuses, there is simply too little opportunity and incentive for junior or senior faculty to lead the charge on pedagogical experimentation. So for now at least, as is often the case in the corporate sector — Kodak and Blockbuster are exemplars that come to mind — the leading edge of disruptive change is primarily being driven by newcomers rather than incumbent leaders. While it is difficult to predict exactly how new technologies, pedagogies and business models will play out over the coming decade, it is a safe bet that those institutions who stubbornly cling to the status quo are likely to find (painfully) that this time it is real: higher education is in the midst of disruptive, transformative change. A former chief technology officer of Hewlett-Packard recently shared the profound observation with me that “the difference between a good idea and a great one is timing.” So true. While (too) much attention is often given to the dangers of being late to market — as HP assuredly was with its ill-fated and short-lived tablet computer — it can be just as deadly to prematurely enter a market before the technology, cost, or operational requirements are ready to deliver a viable consumer value proposition. To put the issue of launch timing in context, recall that every new product launch must overcome three inherent risks to become a market success:

Another example of a great idea in theory, that failed to deliver an attractive value proposition, is the Segway. Hailed as a revolutionary product that would change the world when first introduced by inventor Dean Kaman in 2001, consumers never could figure out why a $3,000 motorized scooter (banned from operating on most big-city sidewalks) made any sense. The world may have changed over the past decade, but largely without the ubiquitous presence of Segways.  Overcoming risks On a brighter note, it is possible to overcome initially negative market reactions to new product concepts, as some of the most successful current products (or those intriguingly on the horizon) demonstrate. Consider the following:

The reasons underlying Apple's success with the iPad have been well documented, including thoughtful design and UI, technical refinement (e.g. battery life, screen resolution), the availability of hundreds of thousands of apps and a huge installed base of step-up iPhone users. All of this boils down to great execution and timing. Steve Jobs had an uncanny sense of not only what, but when to introduce new technology.

Let’s be clear; the world does not need another article pounding Ron Johnson for his ignominious fall from grace. And so I won’t. Except to use this painful episode as a “teachable moment,” rather than just gratuitous schadenfreude. So what have we learned from JCP’s failed strategy? In broadest strokes, it’s that a strategy flawed in both concept and execution has little chance to succeed. Let’s start with a reminder that JCP had to do something to change its game, which is why the Board reached out to a proven executive who had helped transform retailing at Target and Apple. Prior to Johnson’s arrival, JCP had become the somewhat dreary champion of promotion-driven selling, with predictably damaging impacts on the company’s financial performance and image .

By all accounts, Johnson is smart, hard working and decisive and it didn’t take long for the new CEO to stake out a bold and transformative strategy, defined by three major initiatives:

So let’s try throwing Johnson another lifeline. We’ve already noted that Johnson had to take bold, imaginative action. And he’s certainly not alone in radically transforming a sick company by aggressively rolling out an ambitious but largely untested strategy. For example, nearly thirty years ago, Nicolas Hayek raced to implement a national rollout of Swatch in the US, ignoring pilot tests indicating little consumer interest in his boldly fashioned creations from Switzerland. And of course Steve Jobs was famously dismissive about the need for market research or pilot tests before launching massive rollouts of the iPod/iPhone/Tablet. Needless to say, Swatch’s and Apple’s product launches achieved runaway and enduring success. And Ron Johnson was there, at Apple, close to the throne of the master! So little wonder that Johnson would take a page out of Steve Jobs’ (and Hayek’s) playbook to transform JCP by going bold, going big and going fast!! So why are Jobs and Hayek regarded as geniuses and Johnson a goat? Was Johnson just unlucky? On the other hand, maybe Jobs and Hayek were just lucky, and not deserving of their reverential acclaim. Bad luck or bad strategy; which is it? I’ve run out of lifelines and can no longer cut Johnson any more slack. The reality is strategy iscontextual. The fact that a particular strategy worked well in one context most assuredly does not mean that it will thrive in another. There are profound differences between the circumstances surrounding the launches of Swatch and Apple’s innovative consumer entries that simply don’t carry over to JCP’s situation. An understanding of these differences — had JCP taken the time to think it through — would have indicated ex ante that JCP’s commitment to a rapid national rollout of an untested strategy was unwise, unnecessary and breathtakingly risky. Let’s take the flaws in Johnson’s strategy one at a time. 1. The company never demonstrated compelling evidence that JCP’s customers were clamoring for its new strategy; and relatedly, JCP did not or could not articulate the benefits of its strategy in terms that were easily understood by its customers What made JCP think that its consumers hated sales promotions? After all JCP had trained their consumers for over 100 years to expect items on sale. One could surmise that JCP catered predominantly to “bargain hunters” for whom finding an unexpected bargain was part of a game that its customers felt they could always win at JCP. Ron Johnson changed the rules of a game that too many of his customer were enjoying and winning. As same store sales stats soon confirmed, customers either didn’t understand or didn’t like “fair and square pricing”. Either way, they voted with their feet and not their pocketbooks to shop elsewhere. So what is “fair and square pricing?” I put this question to my MBA class this week, and as expected found that JCP had done a poor job clearly communicating its structure and intent. One student correctly suggested that “it had something to do with less reliance on sales promotions.” Fair enough, but to be effective, JCP had to not only say what they were not going to do, but also to clearly explain what made “fair and square” better than what consumers had become accustomed or at least inured to for decades. And on that score “fair and square” pricing turns out to be pretty complicated and confusing. Here’s a primer:

In contrast, consider Swatch’s launch strategy which also was seeking to create a brand centered around value and style. With the acknowledgement that transparent pricing is easier to implement in a company with a few dozen rather than a few thousand SKU’s, here’s Swatch’s pricing approach: All watches — no matter how popular, no matter how new to market, and no matter what rock star designer inspired the creation — will be priced at $40. And that same $40 price tag will stay in force not for one month, or for one year, but for a decade. The same simple price strategy extended around the world, with prices set at 60 DM in Germany and 7,000 Yen in Japan. That’s how you create a brand that meaningfully conveys style and value! One could also argue that by moving its merchandise focus upscale, further away from Sears and WalMart, JCP was distancing themselves from their core customer base in search of new clientele already well served by brands well known for higher quality merchandise — e.g. Macy’s, Bloomingdales and Target. Along with the new pricing scheme, did the JCP really think it its new merchandising strategy would gain more new customers than it risked losing during their strategic transition? Apparently so. 2. JCP raced to implement its strategy on a national scale with no regional pilots to iteratively test and refine new concepts As already noted, there are some inspirational examples of companies that also made big bets on untested big bang launches that paid off. So why pick on JCP on this score? The companies cited earlier operated under three profoundly different circumstances that do not apply to JCP.

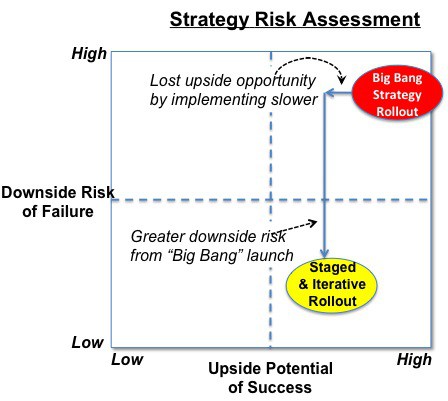

JCP was fighting for current market share within a well defined industry structure, not creating new markets. It’s strategic direction clearly risked alienating its current core customers, and there was no particular reason that the strategy would have been seriously compromised by a more deliberate and staged implementation incorporating testing and iterative refinement. After all, one could argue that Macy’s, Bloomingdales and Target were already occupying the very same space JCP was trying to break into, so there was nothing particularly shocking or new about their brand aspiration. Given JCP’s strategic context, Ron Johnson’s strategy reflected exceptionally poor risk management. Ask yourself this: did the upside potential of a big bang success more than offset the downside risk of failure? As viewed in this risk/reward assessment grid, the answer is decidedly not!  Lessons Learned As a parting shot, two salient lessons learned emerge from the JCP story.

We’ll never know whether Ron Johnson’s strategy would have eventually proved itself in the marketplace, but we do that he ended his career with a bang and unnecessarily put his company in grave peril. Imagine this scenario. Your 103 pound slobbering Labrador Retriever Goofy (name changed to protect the guilty) is sitting around the house one day bored and hungry — a perpetual state of being. For no particular reason (is there ever?), he jumps on the couch and stares at you with a self-satisfied grin. “No! Off!”, you urge, but Goofy stands pat with a defiant tongue dangling well below his jowls. Thinking you can outsmart the beast, you say: “Goofy, do you want a dog bone?” Within nanoseconds, Goofy is at your side, drooling helplessly as you dig a dog bone out of the bin. The next day, Goofy is once again bored and hungry and looks expectantly at you for a treat. But alas, you’re too busy pounding out text messages on your iPhone. Then Goofy gets an idea — when it comes to food, he’s shrewd — and repeats yesterday’s transgression. The plot replays like groundhog day.  Congratulations! You’ve just trained Goofy to jump on the couch whenever he wants a dog bone, which is, like, all the time. This is of course a case of incentivizing the wrong behavior. And business leaders make this same mistake at least as often as dog owners. Why? There tends to be a couple of reasons: 1. Unintended consequences of well intentioned but misguided incentives The first explanation is the most benign. In these cases, managers simply fail to think through the logical consequence of their directives. In retrospect, you may think some of these examples are ludicrous knowing in advance that I’m highlighting incentives that backfired, but I can assure you that each of these situations draws on real world examples — and there are plenty more to choose from.

2. Disingenuous unwillingness to incentivize allegedly desired behaviors Dogs learn early on to watch what their owners do, not what they say. They are after all, dogs. A common example of this same phenomenon in business is when executives disingenuously say the politically correct thing about their priorities but blatantly and knowingly incentivize contrary behaviors. Examples abound.

When there is a clear disconnect between stated objectives and incentivized behavior, institutions lose credibility and authenticity in the eyes of their customers and employees. ******************************************** As I put the finishing touches on this blog entry, my Labrador Retriever is besides me, where else, but on the couch. My protestations not withstanding, I lost credibility a long time ago on canine couch rights with my misguided incentives. In their excellent Harvard Business Review article aptly titled “Big-Bang Disruption”, Paul Nunes and Larry Downes make the case that disruptive new entrants will radically transform more industries far faster than originally envisioned by Clay Christensen in his landmark treatise on this subject 18 years ago. The authors attribute the accelerating pace and scope of disruption to:

With respect to how the new generation of disruptors are likely to impact incumbent market leaders, Nunes and Downes warn: “You can’t see big-bang disruption coming. You can’t stop it. You can’t overcome it. Old-style disruption posed the innovator’s dilemma. Big-bang disruption is the innovator’s disaster. And it will be keeping executives in every industry in a cold sweat for a long time to come.” If you accept this premise (as I do), it leads inexorably to the question every company should be asking themselves: are we innovative enough to be the disruptor and not the disruptee in the next wave of transformational change in our industry? While there are a number of diagnosticsdesigned to test whether companies have a culture conducive to promote innovation, there is one salient indicator that warrants particular attention: how does your company deal with “truth-tellers”? Nunes and Downes define truth tellers as “internal or external seers who can predict the future with insight and clarity. In every industry there are a handful of these visionaries, whose talents are based on equal parts genius and complete immersion in the industry’s inner workings. They may be employees far below the ranks of senior management, working on the front lines of competition and change. They may not be your employees at all. Longtime customers, venture capitalists, industry analysts, and science fiction writers may all be truth tellers.”  Truth tellers play a particularly important role in presaging the need and opportunity to develop new business models which disrupt incumbent business positions, long before the need to change becomes obvious (by which time it’s often too late to stop the destruction of your business by a disruptive newcomer). By their nature, truth-tellers make most business leaders uncomfortable:

Sadly, over a long career in senior management consulting, I’ve witnessed far too many cases where executives not only fail to continuously seek the counsel of truth-tellers, but rather willfully prevent such voices from being heard and evaluated within the organization. What are some of the mechanisms executives use to stifle truth teller input?:

The New York Times carried an ominous story this week on the souring outlook for Barnes & Noble’s Nook business, portending perhaps its exit from the e-reader and tablet markets. The Nook’s decline comes despite its technical competence and the recent infusion of $600 million of capital by Microsoft. As the Times notes, “going into the 2012 Christmas season, the Nook HD, Barnes & Noble’s entrant into the 7-inch and 9-inch tablet market, was winning rave reviews from technology critics who praised its high-quality screen. Editors at CNET called it “a fantastic tablet value” and David Pogue in The New York Times told readers choosing between the Nook HD and Kindle Fire that the Nook “is the one to get.” Unfortunately, high marks from pundits didn’t translate into sales. Nook sales stalled over the Christmas season, losses mounted and profit and revenue guidance has been reduced. What happened? The Times article shares this explanation: “In many ways it is a great product,” Sarah Rotman Epps, a senior analyst at Forrester, said of the Nook tablet. “It was a failure of brand, not product. The Barnes & Noble brand is just very small.” I beg to differ. The Nook’s problems go far beyond B&N’s brand strength. There are three fundamental reasons for Nook’s failure that have implications for any company (and eventually this means every company) facing technology disruption:

2. Disruption redux More broadly the Nook story is yet another example of how disruptive technologies transform value chains, destroying incumbents who no longer create value in the new industry order. With the advent of e-reading devices and digital publishing, book retailers and publishers are severely threatened. We’ve been to this dance before in the music industry, where incumbent retail leaders were essentially wiped out. For a variety of reasons, bookstores (if not the Nook) are likely to survive for quite some time, but only at a fraction of their former scale.Was B&N’s decline inevitable, given the transition from print to digital books? One could ask the same question of Amazon, whose dominance of book sales on amazon.com was equally threatened by e-reader technology. But to Jeff Bezos’ credit, Amazon chose to disrupt itself by aggressively launching the Kindle business, which quickly established itself as the dominant digital book platform. By the time B&N responded with its own Nook devices and e-bookstore, it was too late.The willingness to disrupt one’s own core business before someone else does it to you is a hallmark of inspired leadership. Bezos rules. 3. Stuff Happens! What’s up with Microsoft? As a play on the well known adage, “Disruption Also Happens”! In every industry, the question isn’t whether but only when. The only way to survive and prosper through successive waves of disruption is to be the disruptor, not the disruptee!One would think Microsoft would have learned this lesson by now. Over the past decade, Microsoft has managed to miss five of the most transformative disruptions in the high tech sector:

Bottom line: Serial innovation is the only proven antidote to the accelerating pace of disruptive technologies. It certainly looks like Barnes & Noble and Microsoft have not been up to the task. On June 11, 2012, Tim Cook graced the cover of Fortune Magazine, in a hagiography about the man with perhaps the hardest job in America: to succeed the legendary Steve Jobs who Fortune had already lionized as “the best CEO of the decade” and “the best entrepreneur of our time”  As the Fortune piece noted: “Considering the widespread handwringing over how rudderless Apple would be without Jobs, it is remarkable how steadily the company has sailed along without him.” Time Magazine also weighed in with similar praise: “Highly ethical and always thoughtful, he projects calmness but can be tough as nails when necessary. Like the great conductor George Szell, Cook knows that his commitment to excellence is inseparable from the incredible ensemble he leads at Apple.” Such plaudits certainly seemed warranted at the time. When Fortune’s story appeared, Apple was trading at $571 per share, 52% higher than when Steve Jobs stepped down 10 months earlier. Apple’s stock and was well on its way to cresting at over $700/share in the coming months, prompting Forbes and the New York Times to speculate that Apple — already the most valuable company in the world — was well on its way to becoming the first trillion dollar market capcompany. These were heady times indeed, and Apple and Tim Cook apparently could do no wrong. Or could they? Apple’s fall from grace Less than four months after the Times wondered how soon Apple’s market cap would break the trillion dollar mark, the Wall Street Journal ran a story under the headline “Has Apple Lost Its Cool to Samsung?” CNN had already scooped the Journal, with its own version of: “Is Apple Losing Its Cool Factor?” And what about Tim Cook, the Szell-like conductor of Apple’s innovation band? In mid-January,The Motley Fool asked “Is Tim Cook The Next Steve Ballmer?” which was not meant as a compliment. And two weeks later, Forbes Magazine weighed in with “The Problem with Tim Cook“, raising serious questions about whether Tim Cook was up to the job! What’s going on here?! Sure, there were a couple of missteps with Apple Maps, perceived missing features in the iPhone 5 and the still-unfulfilled promise of Apple iTV. But these events hardly seemed damning enough to signal a cataclysmic reversal of fortune. Can Tim Cook and the company he leads really go from a heavy dose of smarts to serious ineptitude in just four months? Has Apple really lost its mojo and its cool to Samsung, who for so long toiled in the obscurity of Apple’s giant shadow? The Halo Effect Earl Weaver, the Hall-of-Fame manager of the Baltimore Orioles twenty-five years ago opined an answer to these questions, which is as true in business as it is in baseball: “You’re never as bad as you look when you’re losing, nor as good as you seem when you’re winning” There is actually considerable academic research validating Weaver’s sage advice, that falls under the rubric of “The Halo Effect”. In IMD Professor Phil Rosenzweig’s excellent book of the same name, the Halo Effect is defined as the consistent tendency for people to ascribe positive ratings (particularly on subjective assessments like “executive vision” or “leadership”) when the overall measurable performance of a company is good, while tending to be overly critical of management when business outcomes display signs of weakness. One can see this for example in the glowing praise of successful business leaders (such as Reed Hastings of Netflix, Fortune’s 2010 CEO of the year) as “visionary, dynamic and customer-focused”, only to have the very same CEO widely vilified as “complacent, arrogant and unwilling to respond to customer preferences” one year later when the company’s financial performance stumbled. The Halo Effect probably hit bottom for Hastings when SNL parodied him in a bitingly funny skit in 2011. ABB’s Percy Barnevik, GE’s Jack Welch and Groupon’s Andrew Mason are other examples of executives who have felt the sting of hyperbolic punditocracy. It’s fair to say that Tim Cook is the latest victim of the Halo Effect – neither worthy of his early sanctification, nor deserving of his asserted fall from grace. As usual, the business press has been too quick to praise and condemn a man who, in reality has not changed the very essence of his being in just four months! Let’s get real So what can we expect from Apple in the months and years ahead? In my view, there are two parts to answering this question:

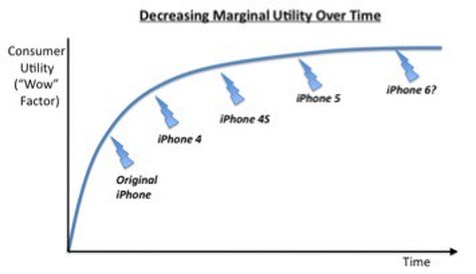

But as good as any of these products are, the simple fact remains that over time, continued improvements yield marginally decreasing utility to consumers. Take Apple’s biggest success to date for example, the iPhone. When the first generation iPhone went on sale in the summer of 2007, it was received with unprecedented global enthusiasm, teasingly dubbed by The Economist as “The Jesus Phone”. And no wonder…it’s design, user interface, functionality and apps support were so radically different and better than any other smartphone on the market that it appeared to many to be miraculously conceived! By the time early adopters’ initial two-year contracts were up, Apple had unveiled its next generation iPhone, the 3GS with faster digital download speeds, an improved camera and considerably more apps. And in every year thereafter, Apple continued to enhance the iPhone. The iPhone 4/4S/5 got progressively, thinner, lighter, brighter (displays), faster, better (cameras), and eventually marginally bigger. While each new version was better than the last, none had the breakthrough market impact of the initial iPhone. Economists have long recognized the marginal decreasing utility – more prosaically, the “wow” factor — associated with virtually every product in the market over time.  For example, except for the most extreme technophiles, most consumers hardly notice the latest generation PC, home printer, digital camera or even automobile these days – a far cry from when the first primitive versions of these revolutionary products first hit the market.

Seen in this light, the fact that Apple’s latest iPhone lacks NFC capability or the best-in-class screen size or the highest megapixel camera does not necessarily signal the end of their innovative spirit. Even if an iPhone 6 were released tomorrow with all of these features, it would fail to create the buzz of the first “Jesus Phone”. Relatedly, it’s entirely to be expected that Samsung and others have largely caught up to Apple on most of the features and functions that define state-of-the-art smartphones. If you have any doubt whether this is a unique failing of Apple, just ask BMW how they would compare their vehicles to the best Hyundai has to offer today vs. ten years ago. Competition happens, and no one is suggesting that BMW has lost its edge. Where now? So what will it take for Apple to continue to be, well, Apple? Its unique challenge is not just to stay abreast of the relentless demands for continuous improvement in its current core products — daunting enough against competitors like Samsung, Google and Microsoft. It is to find thenext breakthrough product category that will once again disrupt a large business value chain to Apple’s profound benefit. A rumored rendition of an Apple “iTV” home entertainment ecosystem is probably the most likely possibility. Critics of Apple should realize that epic business disruptions do NOT operate on a predictable product release timetable, and it is clearly premature to condemn Tim Cook for not pulling another blockbuster rabbit from under his hat during his eighteen months as CEO. Expecting Tim Cook to continue Apple’s growth to unprecedented levels on an arbitrarily imposed timetable is simply not a reasonable standard by which to judge CEO performance. While it is still too early to pronounce judgment on whether Apple’s astonishing string of revolutionary product launches has run its course, the clock is definitely ticking. Businesses are constantly seeking new products, services and business models to create widespread market appeal. But one of the mistakes innovators often make is underestimating the challenge of getting consumers to change their behavior and beliefs in order to realize the benefits of a promising new product. Numerous tomes have been written on overcoming this challenge, perhaps most notably by VC Geoffrey Moore, who shares his wisdom on how to move beyond early adopters to reach the mass market in his 1991 classic, Crossing the Chasm. Spoiler alert: Moore notes that most new technology ventures fail to get across the abyss! So how do companies that launch businesses requiring the marketplace to radically rethink their preconceived notions of product attributes get consumers to change their beliefs and behavior? For starters, successful products of this type — either high or low tech — must inherently have a killer value proposition — e.g. the original Apple McIntosh or Timex watch. But the fact remains that lots of products with breakthrough potential fail to gain market acceptance. One of the key lessons learned from a number of products that have crossed the chasm to widespread market appeal is the use of jarring advertising campaigns with explosive imagery to literally blow up consumers’ comfort with old habits and category norms. Here are some of the best examples: 1. The Apple McIntosh Launch, 1984 In this iconic commercial, considered by many to be the best TV spot of all time, a renegade female warrior hurls a sledgehammer that explosively shatters an IMAX-size screen image of an Orwellian dictator, thinly disguised as the leader of the Microsoft evil empire. A picture is worth a thousand words, so if you haven’t seen this ad recently, check it out. Adding to its mystique, this ad was broadcast only once, during the 1984 Super Bowl. YouTube views since measure in the millions.  Adding to its mystique, this ad was broadcast only once, during the 1984 Super Bowl. YouTube views since measure in the millions. ————————————————————————————————————-- 2. The Timex Watch Launch, 1951 In 1951, Timex introduced the world’s first low priced, highly reliable/rugged wristwatch. Prior to Timex’ launch, wristwatches came in only two “flavors”. Most common were high-priced timepieces utilizing precious jewels in the mechanical movements and casing. Watches of this type were sold exclusively through jewelry stores at prices in excess of $300. These luxury products defined the wristwatch category for many generations, and were often considered family heirlooms. On the other end of the spectrum, watchmakers’ attempts to create lower priced alternatives with cheaper materials generally yielded poor quality, unreliable substitutes, largely shunned by consumers. Timex developed a way to produce low-cost mechanical movements that used hard alloy metals in place of jewels. These new alloy bearings not only lowered the cost of goods, they made automated production easier, further lowering costs. The net result was an extremely accurate and rugged wristwatch sold by drugstores and mass market outlets at prices as low as $6.95! The problem facing Timex was how overcome consumers’ preconceived notion that cheap watches connoted shoddy quality. How did they do it? Once again by blowing up prevailing consumer views with a successful ad campaign under the banner “Takes A Lickin’ And Keeps On Tickin’ “. In each of these ads, a Timex watch was exposed to a draconian torture test (some on live television!) to demonstrate the accuracy and ruggedness of the product. Take a look at this vintage clip for example, where a Timex is strapped to the tip of an arrow and shot by a bowman through a pane of glass (the shattering glass motif, redux), into a wall before dropping into a fish tank filled with water.  Needless to say, Timex watches always survived the lickin’ and kept on tickin’! By literallyshattering the prevailing consumer image of cheap watches , Timex emerged as the market leader, selling one out of every three watches in the US by the end of the 1950’s. ————————————————————————————————————-- 3. SodaStream Banned Super Bowl Ad, 2013 Fast forward to Super Bowl 47 in 2013. One of the game’s ad sponsors — SodaStream — made quite a splash literally and figuratively by having its ads banned by CBS. What was considered a banish-able offense by the game’s broadcaster? See for yourself. SodaStream’s use of exploding glass — in this case bottles of Coke and Pepsi (themselves perennial heavy advertisers of the Super Bowl) — underscores Sodastream’s marketing challenge. Generations of consumers have been brought up consuming soft drinks from bottles whose signature design are an American icon. To communicate the benefits of a radically different approach to soft drink home consumption, SodaStream used — you guessed it — the exploding glass motif to blow up consumers’ prior behavior and beliefs.  Within a week of the Super Bowl, Sodastream’s banned ad had been seen by almost 5 million viewers on YouTube. And the company’s sales have been recently growing by ~50% per year, so obviously SodaStream’s message is getting through to the marketplace. ————————————————————————————————————-- 4. IKEA Unböring Ads, 2003 In 2003, IKEA unveiled its “Unböring” campaign aimed at shattering consumers’ preconceived unflattering notions about home furnishings. The prevailing consumer view was that furniture is boring and shopping is unpleasant — to be avoided at all costs. One market study at the time suggested that Americans tended to change spouses more often than dining room tables! IKEA’s “Unböring” ads jarringly attacked its dreary category image, in one case calling customers attached to their current unstylish furnishings as “crazy”, and in another, having a woman commenting on her bored-to-death furniture and life with the epithet: “That Sucks!”  This latter ad uses more of an implosion than explosion to make the point, but the intent is the same as the other cases noted above: to shatter consumers’ preconceived category norms. Check out the IKEA’s Unböring” ad here.

————————————————————————————————————-- The Bottom Line The lesson learned is that to shake consumers out of old habits and/or preconceived unflattering category norms, companies need to be as innovative in their marketing approach as they are in new product design. No matter how compelling its advantages, if your new product requires consumers to radically rethink their behavior and marketplace beliefs , you will probably need to find ways to jar consumers out of their current mindsets. You may want to look no further than the shattering glass motif to launch your next breakthrough product. |

Len ShermanAfter 40 years in management consulting and venture capital, I joined the faculty of Columbia Business School, teaching courses in business strategy and corporate entrepreneurship Categories

All

Archives by title

How MIT Dragged Uber Through Public Relations Hell Is Softbank Uber's Savior? Why Can't Uber Make Money? Looking For Growth In All The Wrong Places Three Management Ideas That Need to Die Wells Fargo and the Lobster In the Pot Jumping to the Wrong Conclusions on the AT&T/Time Warner Merger What Kind Of Products Are You Really Selling? What Shakespeare Thinks About Brian Williams Are Customer-Friendly CEO’s Bad for Business? Uncharted Waters: What to Make Of Amazon’s Chronic Lack of Profits What Happens When David Becomes Goliath…Are Large Corporations Destined To Fail? Advice to Publishers: Don’t Fight For Your Honor, Fight For Your Lives! Amazon should be viewed as a fierce competitor in its dispute with publisher Hachette Men (And Women) Behaving Badly Why some brands “just don’t get no respect!” Courage and Faustian Bargains Sun Tzu and the Art of Disrupting Higher Education Nobody Cares What You Think! Product Complexity: Less Can Be More Apple's Product Strategy: No News Is Good News Willful Suspension of Belief In The Book Publishing Industry Whither Higher Education Timing Is Everything Teachable Moments -- The Curious Case of JC Penney What Dogs Can Teach Us About Business Are You Ready For Big-Bang Disruption? When Being Good Isn’t Good Enough Is Apple Losing Its Mojo? Blowing Up Old Habits What Is Apple's Product Strategy--Strategic Rigidity or Enlightened Expansion Strategic Inertia Strategic Alignment Strategic Clarity Archives by date

March 2018

|

RSS Feed

RSS Feed