|

Amazon’s Q2 2014 earnings report brought a triple whammy of disappointment to impatient investors:

Three chronic concerns underscore growing investor unease with Amazon’s management priorities:

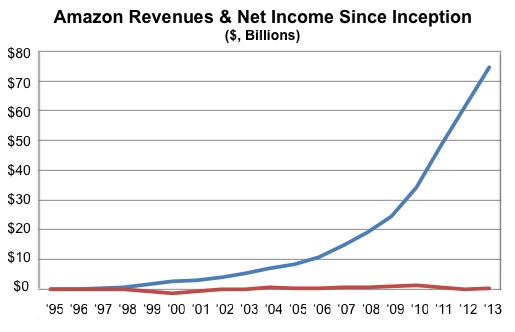

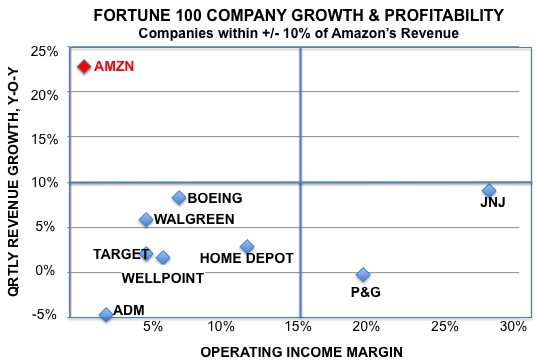

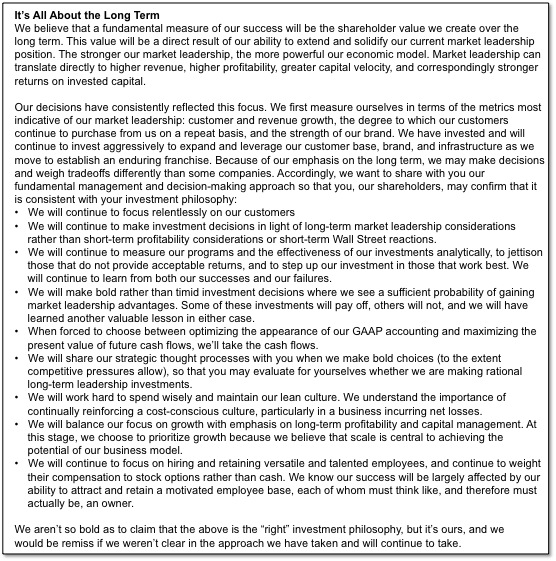

Jeff Bezos’ Guiding Principles Bezos built Amazon on the foundation of being stubborn on vision, but flexible on details. And no CEO has ever been so clear in articulating his corporate vision as Jeff Bezos, who laid out the company’s guiding principles in his first letter to shareholders in 1997. In that document (which Amazon has included in its Annual Report every year since), Bezos signaled his intent to build a company focused on long-term growth, bold action, market leadership and customer satisfaction. As if anticipating the current criticism, in 1997, Bezos cautioned: “Because of our emphasis on the long term, we may make decisions and weigh tradeoffs differently than some companies.” He has been admirably, and to some, frustratingly true to that vision ever since. In this context, let’s examine each of the sources of investor angst in turn. The time is long overdue for the company to deliver profits Echoing the concerns of many analysts, Michael Yoshikami, CEO of Destination Wealth Management (which sold its stake in Amazon last year) recently noted: “Most companies with the kind of gross revenue Amazon has are not posting these kind of losses.” Well that’s an understatement! To put Amazon’s recent financial performance in perspective, consider the figure below, which displays revenue and net income since the company’s inception. There should be little doubt that Amazon has been reinvesting operating profits to fuel future growth. And its growth rate has been extraordinary. From 1995 through 2013, Amazon has grown its topline at a compound annual growth rate of 94%.  Granted, growth rates have slowed as the company has bulked up, but Amazon is on track to be the fastest company in history to reach $100 billion in sales. With current revenues of >$75 billion, Amazon reported 23% topline growth on a year-on-year basis in its Q2 results. As noted below, comparing Amazon to companies that are within +/-10% of its current revenues, Amazon’s topline growth rate is in a class by itself – as is its lack of profitability!  In its relentless pursuit of growth, Amazon has become over-extended Amazon’s profitability has undoubtedly been dragged down by its frenetic pace of investment in new businesses. As Jeff Bezos noted in his official statement accompanying the company’s Q2 earnings report: We’ve recently introduced Sunday delivery coverage to 25% of the U.S. population, launched European cross-border Two-Day Delivery for Prime, launched Prime Music with over one million songs, created three original kids TV series, added world-class parental controls to Fire TV with FreeTime, and launched Kindle Unlimited, an eBook subscription service. For our AWS customers we launched Amazon Zocalo, T2 instances, an SSD-backed EBS volume, Amazon Cognito, Amazon Mobile Analytics, and the AWS Mobile SDK, and we substantially reduced prices. And today customers all over the U.S. will begin receiving their new Fire phones — including Firefly, Dynamic Perspective, and one full year of Prime — we can’t wait to get them in customers’ hands. Each of these ventures requires startup capital that may take years (if ever) to recoup. As Amazon’s cash from operations has grown over time, it has accelerated its investment in new business development, venturing further afield from core ecommerce retailing to compete in the markets for tablets, smartphones, cloud computing, streaming media and original television content. S&P Capital IQ analyst Tuna Amobi (who has a sell rating on Amazon) summed up the sentiment of many in noting: “There’s a lot of stuff they’re doing that’s questionable. There’s nothing wrong with spending to diversify your business, but it has to be in a focused manner as opposed to throwing spaghetti on the wall and seeing what sticks.” The company’s obsessive secrecy manifests a blatant disregard for shareholders, which stands in stark contrast to its customer attentiveness From the company’s founding, Jeff Bezos has been unwilling to divulge financial performance at the business unit level. This has set up a cat-and-mouse game between Amazon executives and industry analysts striving to learn more about company operations. For example, analysts have struggled for years to gain more insight into how many Prime customers Amazon has enrolled, or how many Kindles, Fires, hardcovers or ebooks it has sold, or how much AWS revenue it has booked or how much investment it has made in streaming video. But Jeff Bezos doesn’t like to get specific with numbers. For example, When Bezos took the stage in June to announce the launch of the Amazon Fire smartphone, during his 90-minute presentation, he took the opportunity to drop hints about the company’s broad-based business impact using the deliberately vague terminology: “tens of millions.” Here’s a sampling from his presentation:

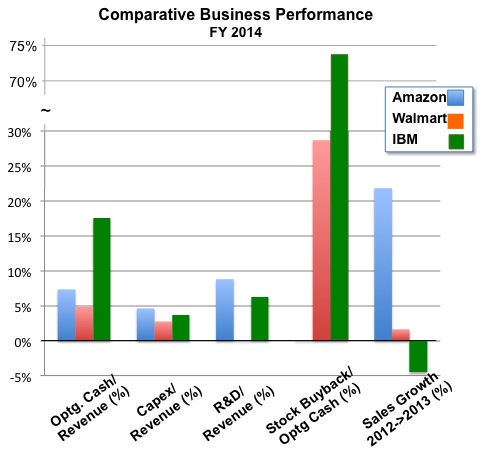

Bezos’ catchphrase is reminiscent of astrophysicist Carl Sagan, who popularized public awareness of astronomy with his frequent reference to the “billions and billions” of stars in the intergalactic universe. The difference of course is that the phenomenon Sagan was referring to is truly unknowable, whereas Jeff Bezos knows precisely how individual components of his business are doing. But that’s for Bezos to know and others to guess.  Care to speculate how many Kindles Amazon has actually sold? From Bezos’ opaque tease, the answer may be 20 million and growing or 220 million but declining. Granted, the SEC doesn’t require public companies to divulge such details to the investment community, but for a company whose market cap has been buoyed by shareholder trust, Amazon’s opacity has been testing investor patience. Every quarter, buy- and sell-side analysts join in a conference call with Tom Szkutak, Amazon’s CFO, and pepper him with questions about company operations. But Szkutak doggedly dodges each query; as exemplified by his replies during Amazon’s Q4 2013 analyst call: “I am sorry I can’t help you … you have to wait on that … In terms of the details, I can’t really give you a lot of color … you will have to stay tuned on that one … I can’t talk to the specifics of that … there is not a lot I can help you with there … I wouldn’t speculate what we would do or not do going forward … I wouldn’t speculate. We might or might not do in the future … if you look back at what we have done, you can’t expect that we might do [it] going forward … I wouldn’t want to speculate what they would or wouldn’t do related to pricing … it’s hard to tell, honestly. It’s hard to know … it’s very early … that’s really all I can say … I can’t comment.” At Amazon, every obfuscating quarterly conference call feels like Groundhog Day. What’s Next for Amazon? So Amazon is arguably guilty as charged of disappointing earnings, worrisome increases in business complexity and investment, compounded by a stubborn unwillingness to share more information about business operations. The market has clearly lost confidence; Amazon is currently trading 25% off its 2014 peak. Does the current market sentiment signal the need for a fundamental shift in Amazon’s overarching business vision, strategy or priorities? I don’t think so. Taking the long view, it is somewhat puzzling that investors have seemingly become so unnerved by Amazon’s recent business performance. There is nothing particularly new or different in Amazon’s business priorities, or in its operating results through the first half of 2014. Jeff Bezos is managing Amazon today exactly as he said he would 17 years ago, making good on his longstanding commitment to prioritize long-term growth and market leadership over short-term financial returns. As such, it shouldn’t be surprising that Amazon has only beat quarterly earnings estimates half the time over the past 20 reporting quarters. So why have investors suddenly become impatient?  Admittedly, there are some headwinds of concern. To begin with, Amazon’s recent EPS misses have come in bunches – viz. 4 out of the last 5 quarters. Then too, some of Amazon’s current business development priorities – cloud computing and original video content development — have particularly high investment thresholds with inherently long paybacks. More generally, the law of large numbers is catching up with Amazon, making the required size of its investment bets and risks higher. Finally, as Amazon has moved farther afield into new business ventures, it has attracted new and stronger competitors. For example, AWS, Amazon’s industry-leading cloud computing business, is encountering fierce price competition from deep pocketed, committed players such as IBM, Microsoft and Google. So it shouldn’t be surprising that Amazon’s historically thin profit margins are under additional pressure. But strategic, growth-oriented companies who are able and willing to sustain new business development activity through cyclical business swings are often rewarded over the long term. As a case in point, Amazon’s relentless focus on new business development and market leadership has propelled its unprecedented long-term growth. Lest there be any doubt that Jeff Bezos is continuing to manage for long-term growth, consider the comparative business performance between Amazon and two of its major competitors: Walmart, the largest global retailer and IBM, a technology leader and fast follower in cloud computing. Where Do The Profits Go? As illustrated below, Amazon performed reasonably well in generating cash from business operations in 2013: 7.4% of revenues compared to 4.9% and 17.5% for Walmart and IBM respectively. What really distinguishes these three large enterprises is how each chooses to deploy their capital. Amazon spends far more of its cash from operations on R&D and Capex – the engines of growth – than Walmart or IBM. The payoff is in topline growth: 23% for Amazon vs. low single digit or negative for its competitors. In contrast, Walmart and IBM reward their shareholders with near term gratification in the form of dividends and stock buybacks (29% and 73% of cash from operations in 2013 for Walmart and IBM respectively).  To understand the reason for these stark differences, it is worth repeating Jeff Bezos’ prescient comments in his 1997 letter to shareholders: “We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions… Because of our emphasis on the long term, we may make decisions and weigh tradeoffs differently than some companies… We aren’t so bold as to claim that [we have] the “right” investment philosophy, but it’s ours, and we would be remiss if we weren’t clear in the approach we have taken and will continue to take.” Virtually every month, Amazon seems to announce yet another major new business venture. Recent examples include Amazon Fresh (groceries), Amazon Local (local services), Get It Now (same day delivery), Amazon Payments (online payments), streaming video and audio services, original content, Fire Smartphone, aggressive expansion in India, etc. Critics who have grown impatient with Amazon’s lack of profits may be underestimating the long gestation period required for new-to-world ventures to yield attractive returns. This was certainly the case with Amazon’s initial ecommerce business, and subsequent third party marketplaces and Kindle platform, which took as long as a decade to go from concept to profitable returns. This is not to suggest that Amazon hasn’t experienced its share of abject failures, including the following initiatives, which either were abandoned, written off or salvaged only via pricey, face-saving acquisitions:

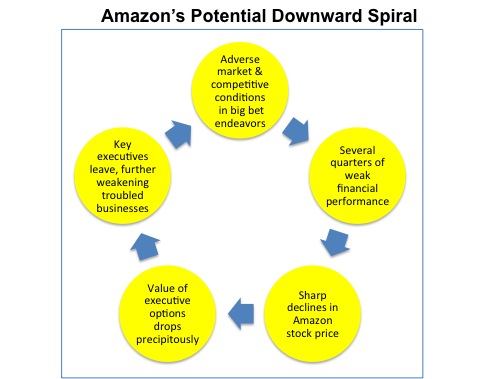

It is also important to recognize that Amazon’s preference for long-term growth over short-term profits is a matter of strategic choice. Amazon could easily boost its EPS by throttling back Capex and R&D investments (at the expense of growth), whereas, it is unclear whether Walmart or IBM are capable of turbocharging their topline growth. Investors who expect Amazon to deliberately scale back its growth initiatives and/or raise prices to achieve short-term profits either don’t understand the company or lack the appetite for Jeff Bezos’ long-term vision. Amazon is positioning itself at the epicenter of multiple businesses with exceptionally strong growth potential – global ecommerce, streaming media, electronic payments, cloud computing, same-day delivery services, the South-Asian continent etc. It is neither in Amazon’s DNA or long-term interest to slow its pursuit of these opportunities. What could go wrong? Is Amazon an indomitable force, bound for world domination? Of course not. There are a number of factors that could sidetrack Amazon’s prodigious appetite for growth and market leadership. The biggest challenge is management risk associated with the growing complexity of Amazon’s global business endeavors. As noted earlier, Amazon chooses to operate with razor thin margins across its business portfolio, and as such, will have to execute flawlessly to maintain torrid growth without jeopardizing their balance sheet. This will require a deep bench of committed executive talent across the enterprise. As their Q3 2014 guidance perhaps presages, Amazon may hit a bad patch if a few of its strategic growth initiatives take longer to materialize, attract more vigorous competition and/or require considerably higher investment than anticipated. Such outcomes, as noted below, could set in motion a downward spiral in business performance that might require significant retrenchment. Amazon relies heavily on options-based compensation in its senior executive ranks, making the company vulnerable to prolonged softness in the stock market. Given its dependence on public markets to fuel aggressive organic growth and acquisitions, Amazon’s reticence and repeated opacity in dealing with the investment community is another risk factor. A growing chorus of analysts and shareholders has lost patience with what they view as the company’s arrogant disregard of shareholders. True, the company can point to its unusual candor in initially articulating its management philosophy and to the shareholder-friendly returns achieved over the past decade (~500% stock price appreciation from mid-2004 to mid-2014). But the public has short a memory span, and Amazon risks needlessly squandering shareholder trust by doggedly refusing to respond to questions regarding business line results or to provide a credible case for the company’s path to profitability.  Another risk factor of course is Jeff Bezos himself. Few companies are as personified by their CEO as Amazon. Bezos’s eventual successor will obviously have some very big shoes to fill, with outsized management transition risk. But for the foreseeable future, with respect to Jeff Bezos’ guiding vision, don’t expect new news from Amazon. If you’re looking for hints on Amazon’s strategic blueprint for the years ahead, look no further than Bezos’ 1997 letter to shareholders excerpted below.

1 Comment

4/18/2019 07:43:07 am

I'm starting to think I need to reconsider my own thoughts on this topic.The points made here are original. I hope you continue this. Your work surpasses my expectations. Your comment will be posted after it is approved.

Leave a Reply. |

Len ShermanAfter 40 years in management consulting and venture capital, I joined the faculty of Columbia Business School, teaching courses in business strategy and corporate entrepreneurship Categories

All

Archives by title

How MIT Dragged Uber Through Public Relations Hell Is Softbank Uber's Savior? Why Can't Uber Make Money? Looking For Growth In All The Wrong Places Three Management Ideas That Need to Die Wells Fargo and the Lobster In the Pot Jumping to the Wrong Conclusions on the AT&T/Time Warner Merger What Kind Of Products Are You Really Selling? What Shakespeare Thinks About Brian Williams Are Customer-Friendly CEO’s Bad for Business? Uncharted Waters: What to Make Of Amazon’s Chronic Lack of Profits What Happens When David Becomes Goliath…Are Large Corporations Destined To Fail? Advice to Publishers: Don’t Fight For Your Honor, Fight For Your Lives! Amazon should be viewed as a fierce competitor in its dispute with publisher Hachette Men (And Women) Behaving Badly Why some brands “just don’t get no respect!” Courage and Faustian Bargains Sun Tzu and the Art of Disrupting Higher Education Nobody Cares What You Think! Product Complexity: Less Can Be More Apple's Product Strategy: No News Is Good News Willful Suspension of Belief In The Book Publishing Industry Whither Higher Education Timing Is Everything Teachable Moments -- The Curious Case of JC Penney What Dogs Can Teach Us About Business Are You Ready For Big-Bang Disruption? When Being Good Isn’t Good Enough Is Apple Losing Its Mojo? Blowing Up Old Habits What Is Apple's Product Strategy--Strategic Rigidity or Enlightened Expansion Strategic Inertia Strategic Alignment Strategic Clarity Archives by date

March 2018

|

RSS Feed

RSS Feed